Last Updated on March 3, 2026 by Shrestha Dash

In the last five years, publicly reported ERP implementation failures have exceeded $1 billion in documented financial losses. Industries include corporate, healthcare, manufacturing, and government sectors. That figure only includes cases where costs were publicly quantified; the true total is significantly higher. What makes this data particularly striking is not the absolute scale of loss. It is that the failures are occurring at organizations with substantial resources. Also, they have access to tier-1 implementation partners and full visibility into decades of documented failure patterns.

The ERP implementation failure lessons have been available since Nike’s 2001 supply chain collapse became a Harvard Business School case study. Hershey’s 1999 Halloween disaster is read in supply chain management programs. National Grid’s SAP stabilization program, widely reported to cost hundreds of millions to over a billion dollars, depending on accounting scope. And yet, in 2024 alone, a medical device company filed a $172 million lawsuit against its implementation partner. A food manufacturer lost $135 million in revenue in a single quarter. Also, multiple US cities left thousands of public sector workers without correct pay.

The ERP implementation failure lessons are not new. What is new is the scale of consequence, the speed of financial impact, and the addition of an entirely new failure mode. It is securities litigation: something that the earlier generation of ERP disasters did not face. This blog examines the cases with specific detail and cross-case comparison that turns documented disasters into actionable intelligence.

Why the Failures Are Getting More Expensive, Not Less

Before diving into individual cases, it is worth confronting the uncomfortable question directly: why is this still happening, and why at greater cost?

Three structural shifts explain the escalation:

- Procurement teams are systematically ignoring the warnings. Every major implementation partner and ERP vendor publishes implementation methodology guides. The failure patterns are public record in industry journals, legal filings, and audit reports. And yet organizations continue to sign contracts with milestone-based fee structures that incentivise SI speed over quality, proceed with go-live against internal readiness warnings, and treat data migration as a background task rather than a program gate. The ERP implementation failure lessons are available. The discipline to apply them is not.

- The complexity ceiling has risen dramatically. Organizations moving to SAP S/4HANA, Oracle Fusion Cloud, or Workday in 2024 are not just replacing a legacy system. They are consolidating multiple legacy systems, migrating decades of accumulated data, integrating with increasingly complex third-party ecosystems. And doing all of this while the underlying cloud platforms are still maturing. Zimmer Biomet was attempting to consolidate nine legacy ERP systems into one. Lamb Weston was replacing a decades-old system across a multi-site, multi-distributor network in real time. The technical surface area for failure has grown.

- The financial stakes of go-live are higher. When operational systems fail today, the consequences hit faster and harder than they did twenty years ago. A medical device company that cannot ship products, generate invoices, or produce sales reporting does not just inconvenience customers. It misses guidance, moves markets, and creates securities disclosure obligations. The financial system has become so tightly coupled to operational execution that ERP implementation failures now have capital market consequences. Also, this simply did not exist for the previous generation of failures.

Zimmer Biomet vs. Deloitte Lawsuit

Zimmer Biomet’s SAP S/4HANA implementation has been widely covered as a cautionary tale of ERP failure. The September 2024 lawsuit filing against Deloitte, however, transforms the case from industry discussion into a documented legal record. Along with specific allegations that every organization planning an ERP implementation should examine carefully.

What the Lawsuit Actually Alleges

Zimmer Biomet filed a lawsuit seeking approximately $172 million in damages against Deloitte in September 2024. This a medical device manufacturer with approximately $8 billion in annual revenue. The company’s general counsel stated that disruptions “not only seriously disrupted our business, but also put patient care at risk.” That last phrase matters. For a medical device company, ERP implementation failure is not just a financial event — it has regulatory and patient safety implications.

The specific allegations in the lawsuit go well beyond “the system didn’t work”:

- The warehouse management module was designed, configured, and implemented in a manner that allegedly ruptured Zimmer Biomet’s supply chain. Thus, leaving the company unable to ship or receive products, generate invoices, or produce accurate sales reporting for extended periods

- Offshore resource model with constant turnover — the lawsuit alleges heavy reliance on offshore resources in India with a revolving door of personnel, meaning continuity of knowledge across build, integration, testing, and go-live phases was structurally compromised

- Contract analysis published indicates that more than 50 change orders totaling approximately $94 million were processed before the system even launched. Thus, approximately a 36% overrun on the original $69 million contract. Each change order represents a scope or specification that was wrong or missing at contract signing

- Go-live slipped five times — from February 2023 to July 4, 2024 and proceeded at the sixth attempt despite indicators that the system remained unready

- The lawsuit alleges tens of millions of dollars in additional internal remediation costs beyond amounts paid to Deloitte, with the system still reportedly suffering from significant defects, functionality gaps, and performance issues at the time of filing

The Contract Structure That Created Misaligned Incentives

This is the ERP implementation failure lesson from Zimmer Biomet that most analyses miss entirely. The lawsuit shows that Deloitte tied approximately $50 million of its $63 million in fees to time-based milestones rather than measurable business outcomes.

Think about what that means structurally. An SI that earns its fees by hitting dates has a financial incentive to hit dates. It does not have a financial incentive to delay go-live when internal signals suggest the system is not ready. It does not have a financial incentive to escalate readiness concerns that might trigger a delay. The ERP contract structure created a situation where Deloitte’s financial interest and Zimmer Biomet’s operational interest were in direct conflict at every go/no-go decision point.

Add to this a 25-year sole-source relationship with Deloitte, meaning Zimmer Biomet had never run a competitive procurement for this scope and you have a governance structure that had systematically eliminated independent challenges at every level.

The Securities Dimension

CEO Ivan Tornos disclosed operational disruptions at the Wells Fargo Healthcare Conference in September 2024, quantifying revenue impact at approximately $75 million annually. The company subsequently revised that figure to $54 million across Q3 and Q4. Stock price dropped over 8% on the disclosure day. The lawsuit alleges that the disruption coincided with a multi-billion-dollar decline in market capitalization.

When a publicly traded company makes statements about ERP system readiness or about the absence of material operational impact and those statements prove inaccurate, the ERP implementation failure becomes a securities law event. The CIO, Zeeshan Tariq, exited in October 2024 during remediation. The full-year 2024 revenue guidance was reduced. Adjusted EPS guidance was cut.

The ERP implementation failure lesson here is specific and contractual:

- For publicly traded companies, external legal counsel should review ERP readiness assessments for securities disclosure implications before the company makes any public statement. A $135 million revenue loss in one quarter creates perhaps $500 million in destroyed market capitalization, but the sustained underperformance relative to sector peers over 18+ months creates billions more in foregone equity value.

- Fee structures should link payment to measurable business outcomes, not time-based milestones

- Competitive procurement should be mandatory even for long-standing SI relationships

- Go/no-go authority should sit with an independent party, not solely with the program team and SI

ERP Selection Requirements Template

This resource provides the template that you need to capture the requirements of different functional areas, processes, and teams.

Lamb Weston $135 Million Loss

Lamb Weston Holdings is not a company most people outside the food industry would recognise. It is, however, North America’s largest frozen potato products producer, supplier of approximately 15% of McDonald’s annual sales, and the company that posted one of the fastest-onset ERP-driven financial collapses in recent corporate history.

The Q3 FY2024 Numbers

When Q3 FY2024 results were announced on April 4, 2024, the figures were staggering in their specificity:

- $135 million in lost net sales directly attributable to the ERP implementation

- $72 million reduction in net income in a single quarter

- $95 million decrease in adjusted EBITDA

- Volume decline of 16% in the quarter, with approximately 8 percentage points attributed directly to ERP

- $25 million in inventory write-offs for excess raw potatoes that the system failed to manage

- Full-year revenue guidance slashed by $330 million at the midpoint

- The stock fell nearly 20% in a single trading session following the disclosure.

To put that in context: a single SAP S/4HANA go-live event in late November 2023 erased more than a fifth of the company’s market value within four months.

The Operational Mechanism Failure

The failure mechanism at Lamb Weston is instructive because it is so precisely documented. The ERP transition temporarily eliminated visibility of finished goods inventories at distribution centres. Without accurate inventory visibility, the company’s order fulfilment capability collapsed, particularly for higher-margin customers with complex, mixed-product orders requiring accurate stock allocation across multiple locations.

The company was forced to deploy team members physically to distribution centres to manually resolve data errors in real time. This is not a workaround – it is an admission that the integration between SAP and third-party warehouse management systems had failed at a fundamental level, and that the fallback was human bodies replacing automated processes.

This did affect the higher-margin, higher-complexity orders. This is a pattern that repeats across ERP implementation failures: the most complex business processes, which also tend to be the highest-value ones, are exactly the processes that expose integration and data failures first, because they exercise more of the system’s logic simultaneously.

The Governance Failure That Compounded the Damage

The operational failure, as significant as it was, was compounded by a governance failure that is worth examining independently. On the January 2024 earnings call, Lamb Weston’s CFO characterised early issues as “the usual bumps associated with these highly challenging large-scale projects” and stated the company did not expect the cutover to have a material impact on full-year results.

That statement became central to subsequent securities class action lawsuits, with plaintiffs alleging the company knew the system was not ready to go live but proceeded, and then knowingly mischaracterised the severity of the operational impact to investors.

A new CIO, Benjamin Heselton, was appointed in October 2024. The company modified its entire deployment strategy, from simultaneous multi-site rollout to sequential plant-by-plant implementation. That revised approach is what the program should have been from the start.

The ERP implementation failure lessons from Lamb Weston are sequential:

- Before go-live: Multi-site simultaneous deployments amplify risk exponentially. Sequential rollout with lessons-learned gates between each site is the lower-risk architecture, always

- At go-live: Inventory visibility testing between the new ERP system and all third-party warehouse systems should be a formal go-live gate with defined pass/fail criteria — not an assumption

- After go-live: Investor communications about ERP readiness and operational impact require legal review. Characterising known, documented issues as “usual bumps” when material financial impact is already measurable creates securities litigation exposure

- During procurement: Simultaneous multi-system cutover for a company of this supply chain complexity should have been challenged — ideally by an external party not commercially invested in the timeline

ERP System Scorecard Matrix

This resource provides a framework for quantifying the ERP selection process and how to make heterogeneous solutions comparable.

Workday Government Payroll Cascade

Workday government payroll failures have generated substantial industry discussion. What Seattle’s February 2025 class-action lawsuit reveals, however, transforms the narrative from individual failures into a systemic accountability crisis. The pattern is not just that these ERP implementations failed. It is that the failures were documented, publicized, and explicitly communicated to subsequent implementers, who proceeded anyway.

The Cascade From Oregon to Seattle

The timeline of Workday government payroll failures tells a story of documented warnings that were consistently overridden:

- Oregon (December 2022): A $21 million Workday system affects 44,000 state employees. In the first January 2023 pay period, approximately 4,500 employees, 10% of the workforce, are underpaid or overpaid. Over 2,000 additional workers received incorrect pay in subsequent periods. Employees use food banks and borrowed money to cover the gap. State auditors find that testing was “either not sufficiently scoped or not properly conducted.” A $15 million class-action settlement follows.

- Maine (terminated 2021): $34.7 million spent over five years on a Workday implementation that is abandoned entirely. Testing revealed payroll calculation error rates exceeding 50%. An independent assessment finds that legacy payroll data was filled with errors and inaccuracies accumulated over decades – the new system did not create the problem, it exposed it. Maine had previously failed with a $13.5 million Infor implementation in 2016. Two platform failures in under a decade signal an organizational data governance problem that no software vendor can solve.

- Los Angeles (September 2024): Go-live immediately leaves approximately 14,000 municipal employees underpaid, overpaid, or unpaid. Total costs reach $94 million against an original $62.1 million budget. By July 2024, the city has logged 5,841 support incidents with a steadily increasing resolution backlog. Payroll complexity is described in city documents as involving over 1,500 salary formulas across diverse departments.

- Seattle (September 2024, lawsuit filed February 2025): The city’s Workday go-live in the same month as thousands of municipal employees were underpaid, overpaid, or unpaid following go-live. Named plaintiffs include a 12-year engineering supervisor, a 28-year firefighter, and a 15-year police sergeant. Allegations include pay rates adjusted downward by $20 per hour for some workers, missing leave accruals, and deferred compensation that vanished from records. The lawsuit alleges that Seattle had been warned directly about the Oregon, Maine, and Los Angeles failures — and proceeded on the same timeline regardless.

Why Government Payroll Is the Hardest ERP Environment

The Workday failures are not Workday-specific; they are environment-specific. Government payroll systems operate in the most complex pay calculation environment that exists:

- Multiple simultaneous union contracts, each with distinct overtime formulas, shift differentials, hazard pay rules, and leave accrual structures that interact with each other

- Hundreds or thousands of individual salary classifications that each carry unique pay rules built up over decades of collective bargaining

- Regulatory obligations that make payroll errors legally consequential, not just operationally inconvenient, for both the organisation and the employee

- Legacy systems that have accumulated 20–30 years of exceptions, manual overrides, and undocumented workarounds that front-line payroll staff know intimately but that no requirements document has ever fully captured

When a new system goes live in this environment without exhaustive parallel running, processing at least two complete pay cycles on both the old and new systems simultaneously, and reconciling every discrepancy before cutover, the probability of payroll errors is not a risk. It is a near-certainty.

The Specific ERP Implementation Failure Lesson

The most significant ERP implementation failure lesson from the Workday cascade is not about platform capability or data quality. It is about institutional learning or the absence of it. Seattle’s project team had documented access to the Oregon failure findings, the Maine abandonment report, and the Los Angeles implementation challenges. They proceeded on an identical timeline to Los Angeles, with identical go-live results.

This points to a procurement and governance failure that precedes the implementation itself:

- Organizations should complete legacy data audits and resolve all historical calculation errors before migration begins, rather than discovering them during go-live

- Independent pre-implementation assessment of comparable organization failures should be a mandatory procurement gate, not optional reading for the project team

- Parallel payroll running for a minimum of two complete cycles should be a contractual non-negotiable in any government payroll implementation, regardless of vendor or timeline pressure

- Union and employee representative engagement in testing and validation is not a change management nicety; in a unionized environment, it is a risk management necessity

The Three Things That Are New About These ERP Failures

Analysis of ERP implementation failures from earlier decades identified classic failure factors: vendor selection issues, inadequate planning, insufficient change management, governance weakness, and timeline pressure. All of those apply to the cases documented above. But the 2024–2025 failures introduce three dimensions that represent a genuine escalation beyond historical patterns.

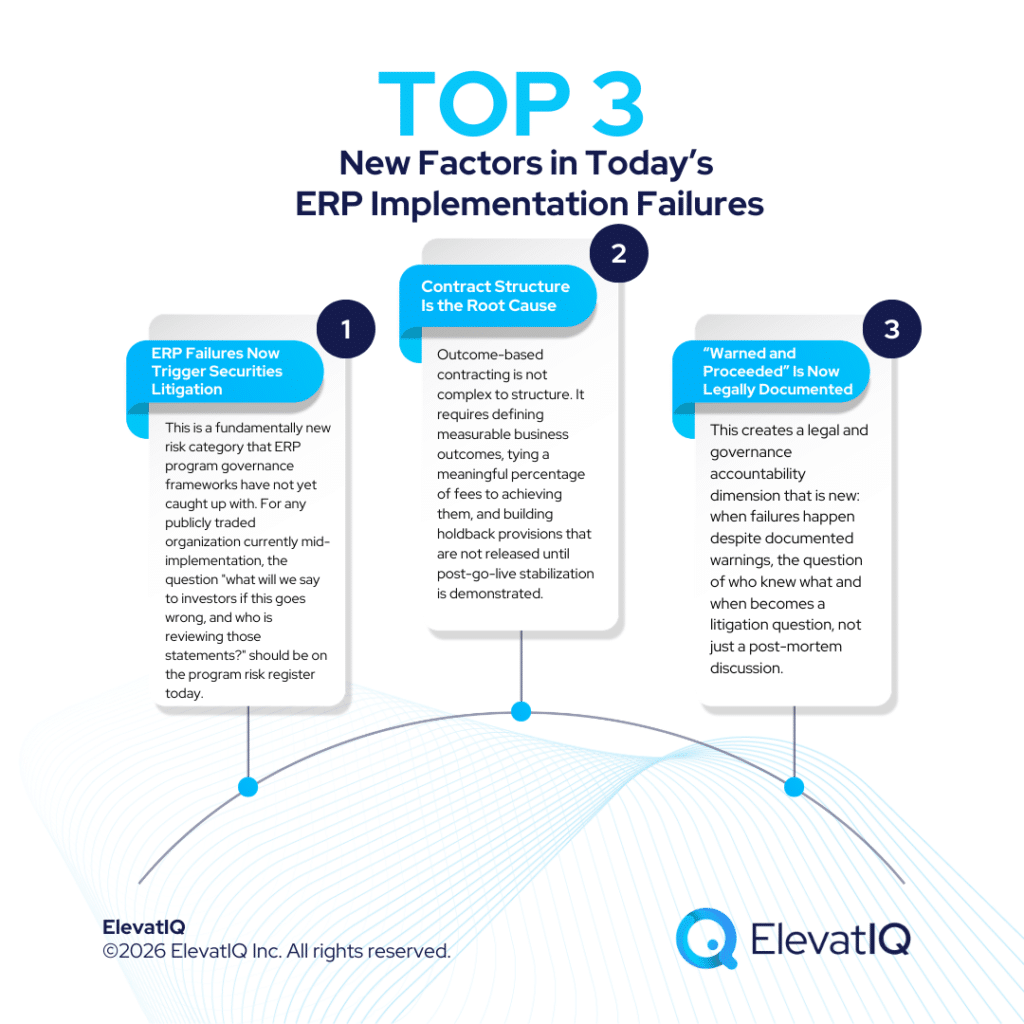

Securities Litigation Is Now a Standard Consequence of ERP Failure for Public Companies

Zimmer Biomet and Lamb Weston both faced securities class action lawsuits as a direct consequence of their ERP implementations. In both cases, the allegation is not just that the system failed, but that the company made public statements about system readiness or operational impact that proved materially inaccurate.

This is a fundamentally new risk category that ERP program governance frameworks have not yet caught up with. For any publicly traded organization currently mid-implementation, the question “what will we say to investors if this goes wrong, and who is reviewing those statements?” should be on the program risk register today.

The Contract Structure Is the Root Cause, Not Just a Contributing Factor

Zimmer Biomet’s lawsuit makes explicit what has been implicit in previous failures: a contract structure that ties SI fees to time-based milestones rather than business outcomes structurally misaligns the SI’s financial interest with the client’s operational success. This is not a governance oversight. It is a procurement decision with a predictable consequence. Outcome-based contracting is not complex to structure. It requires defining measurable business outcomes, tying a meaningful percentage of fees to achieving them, and building holdback provisions that are not released until post-go-live stabilization is demonstrated.

The “Warned and Proceeded” Dynamic Is Now Legally Documented

Seattle’s case is the clearest example, but the pattern exists in Zimmer Biomet (five delayed go-lives, proceeded at the sixth), Lamb Weston (CFO characterized known issues as “usual bumps”), and Los Angeles (documented awareness of Oregon and Maine failures). In each case, the organization had access to warning signals that should have triggered either delay or course correction and did not act on them.

This creates a legal and governance accountability dimension that is new: when failures happen despite documented warnings, the question of who knew what and when becomes a litigation question, not just a post-mortem discussion.

What Organizations Currently Planning ERP Implementations Should Do

Given what the 2024–2025 cases add to the ERP implementation failure lessons already on record, here is what every organization currently in planning or procurement should be doing differently:

Contract structure:

- Insist on outcome-based fee provisions and tie a meaningful percentage of SI fees to defined business outcomes measured 90–180 days post go-live, rather than to milestone completion dates

- Release explicit holdback provisions only after the organization meets post-go-live stabilization criteria

- Run a competitive procurement even if you have a long-standing SI relationship; the competitive process validates approach, staffing quality, and pricing in ways that sole-source arrangements cannot

Investor communications (for public companies):

- Add “ERP readiness and investor communication” as a standing item on the program risk register from program inception

- An external legal counsel should always review any public statement about ERP readiness, go-live progress, or operational impact before publication

- Establish a disclosure protocol agreed between the program director, CFO, general counsel, and investor relations before go-live, not after problems emerge

Multi-site and government deployments:

- Sequential rollout is not a conservative option, it is the correct architecture for any complex multi-site or multi-system environment

- Organizations must treat parallel running for payroll and financial systems as a non-negotiable requirement, not as a best practice to trade off against timeline pressure

- Before migration design begins, organizations should complete legacy data audit and error remediation, not during it

Learning from documented failures:

- Require the program team to produce a written analysis of comparable organization failures as part of the pre-implementation ERP readiness assessment

- Engage an independent reviewer to challenge program assumptions against the documented failure record, not just against the SI’s implementation methodology

The Conclusion

The $1 billion in documented ERP implementation failure costs from 2020–2025 does not represent a failure of knowledge. The ERP implementation failure lessons from Zimmer Biomet, Lamb Weston, and the Workday government cascade are the same lessons that were available from Nike, Hershey, FoxMeyer Drug, and every other major failure that preceded them. What is new is the scale of consequence and the addition of securities litigation as a standard downstream risk for public companies.

Industry case studies often cite organizations such as Discover Financial Services and Evergreen Garden Care as examples of more successful ERP programs. They have different governance disciplines: realistic timelines built from evidence rather than aspiration, data readiness standards enforced as gates rather than guidelines, contract structures that align SI incentives with client outcomes, and independent challenge at every stage of the program lifecycle.

That last element, independent challenge, is where independent ERP advisors provide value that internal teams and commercial SIs are both structurally unable to provide themselves. An SI has a financial interest in the program proceeding. An internal team operates under the organizational pressures that produced the problematic decisions in the first place. Independent advisors carry the pattern recognition of organizations that have seen these failure modes repeatedly, the credibility to challenge program assumptions that internal governance cannot, and no commercial stake in the go-live date.

If your organization is planning an ERP implementation, mid-program, or showing early warning signs of any of the patterns described in this blog, the team at ElevatIQ works with organizations at exactly these inflection points — before the losses become headlines.

(All commentary and analysis represent an independent editorial perspective based on publicly reported information and cited primary sources.)

ERP Selection: The Ultimate Guide

This is an in-depth guide with over 80 pages and covers every topic as it pertains to ERP selection in sufficient detail to help you make an informed decision.

FAQs

Related Posts: