Last Updated on May 4, 2026 by Shrestha Dash

In the first week of November 2025, Tennant Company (NYSE: TNC) cut over to a new company-wide SAP cloud-based ERP system in North America. It is a Minnesota-based global manufacturer of industrial cleaning equipment, with approximately $1.3 billion in annual revenue. Within days, the business could no longer reliably process or ship customer orders.

The financial damage disclosed on February 24, 2026, was immediate and concrete. They were as follows:

- Approximately $30 million in lost net sales in Q4 2025

- A $22 million reduction in Q4 adjusted EBITDA

- Over $20 million in unplanned remediation costs for 2026, against an original remediation budget of roughly $5 million

- Gross profit margin collapsing from 41.3% in Q4 2024 to 34.6% in Q4 2025

- Tennant’s stock falling 23.4% in a single trading session, from $82.30 to $63.02. Thus, erasing approximately $343 million in market capitalization

- The EMEA go-live, previously scheduled for the following quarter, paused indefinitely

The combined revenue and EBITDA impact in a single quarter was approximately $52 million. The total ERP program investment since 2023 reached approximately $98 million. Multiple securities law firms launched investigations into whether Tennant had accurately represented the project’s progress and risk to investors before the North American disclosure.

An ERP go-live failure of this scale from a company that appeared to follow standard ERP implementation practices, phased its rollout, and acknowledged project risk publicly deserves close examination. Tennant had flagged the project publicly for years. It has acknowledged the risks openly and followed what appeared to be industry best practice in phasing the rollout geographically. The company assessed the Asia-Pacific deployment in September 2025 as successful. Then, it followed with a North American go-live described as extensively prepared. And it still failed.

The Setup: A Legitimate Transformation with a Sound Rationale

Tennant’s ERP consolidation was not an opportunistic initiative. In the Q4 2023 earnings call, CEO Dave Huml articulated the rationale directly. The company was running eight separate ERP systems globally on aging infrastructure. He described that consolidating them onto a single SAP cloud-based platform was essential to the company’s three-year growth strategy. The company estimated the program would cost approximately $75 million in total capital and operating expenditure through 2025, with around $37 million expected in 2024 alone.

The case for consolidation was well-reasoned. Eight fragmented ERP instances make data visibility, operational efficiency, compliance, and cybersecurity governance significantly more difficult to maintain. Bringing the entire enterprise onto a unified platform addresses all of those problems simultaneously.

Throughout 2024 and into 2025, Tennant provided investors with regular progress updates. The company characterized the project as “progressing as we’ve anticipated” and “on time and on budget.” By Q3 2025, it had completed the Asia-Pacific go-live and described it as successful. It had North America underway and scheduled EMEA for the following quarter. Then the Q4 2025 results hit. The ERP go-live failure in North America significantly offset the efficiency gains the consolidation program was designed to deliver over time.

What Actually Went Wrong

In CEO Dave Huml’s own words from the Q4 2025 earnings call:

“Despite a successful go-live in the APAC region in September and extensive preparation in North America, the cut-over of the ERP system in the first week of November introduced severe system functionality issues that limited our ability to enter orders, ship products, and service our customers.”

Three operational functions failed simultaneously at go-live: order entry, product shipment, and customer service. For a manufacturer whose revenue model depends on processing equipment orders and delivering them reliably, this is a failure in the core of the business, not in a peripheral administrative function.

The scale of the disruption indicates this was not a brief cutover hiccup that self-corrected within days. Stabilization challenges extended well beyond the initial go-live window, requiring significant additional investment. The 4x overrun on the original remediation budget is the clearest evidence of that. The company has paused the EMEA deployment indefinitely while North America continues its recovery.

ERP Selection Requirements Template

This resource provides the template that you need to capture the requirements of different functional areas, processes, and teams.

Why the Asia-Pacific Success Did Not Predict the North American Failure

One of the most instructive aspects of the Tennant case is the regional asymmetry. The Asia-Pacific rollout was assessed as successful in September 2025. Eight weeks later, the North American go-live failed.

Organizations commonly observe this pattern in phased ERP programs: earlier phases succeed, while the largest and most complex region experiences ERP go-live failure. Several structural factors explain it:

- Transaction volume and complexity. North America is typically the largest revenue region for a global manufacturer. It concentrates the highest order volumes, the densest customer base, and the most complex fulfillment workflows. A system that processes APAC-scale transaction loads without incident may surface entirely different failure modes when exposed to North American peak volumes.

- Integration depth. The number of systems, processes, and dependencies connected to the ERP grows with operational scale. North American operations typically carry more integration complexity, more third-party logistics connections, more distributor relationships, more legacy system touchpoints, than earlier-phase deployments.

- Process variability. Even within a single ERP program, process configurations differ meaningfully across regions. Workflows validated in APAC may not accurately represent the configuration paths used in North America, meaning that testing results from the earlier go-live carry limited predictive value for the later one.

- Cutover execution at scale. The mechanics of cutover including data migration, parallel running, fallback procedures, become materially more complex at North American scale than at APAC scale. Issues that are manageable at a smaller scale can cascade at a larger scale.

As noted in its analysis: phased rollouts do not eliminate risk, they redistribute it. Success in one region does not guarantee stability at scale, particularly when process and geography variability and operational complexity increase significantly in subsequent deployments.

ERP System Scorecard Matrix

This resource provides a framework for quantifying the ERP selection process and how to make heterogeneous solutions comparable.

The Investor Communication Dimension: A New Category of ERP Risk

The Tennant case introduces a risk dimension that most ERP implementation guides do not address: investor communication liability.

Following the February 24 disclosure, securities law firms including Bleichmar Fonti & Auld LLP and Hagens Berman launched investigations into whether Tennant’s prior statements about the ERP rollout accurately represented the project’s progress and risk. The central allegation is that the company characterized the project as on track and the Asia-Pacific go-live as successful in its investor communications, while North America was experiencing or heading toward problems that those communications did not reflect.

These are investigations, not proven findings. They do not establish wrongdoing. But their existence and the speed with which they were launched highlight an important structural point: publicly listed organizations now recognize ERP implementations as material business events subject to the same disclosure expectations as financial restatements and operational incidents.

The gap between internal awareness of ERP go-live failure risk and external communication of that risk is no longer purely a reputational concern. It has become a legal one. For enterprise leaders, including those at privately held companies, where the audience is lenders, private equity sponsors, or boards rather than public investors, the broader principle applies: governance structures must ensure that decision-makers receive timely, honest program health reporting rather than filtered status updates calibrated to maintain organizational momentum.

Five Lessons Enterprise Buyers Must Apply

The Tennant ERP go-live failure is not an isolated anomaly. It reflects failure patterns that appear consistently in large-scale ERP programs. Each of the following lessons is directly traceable to what the Tennant case reveals.

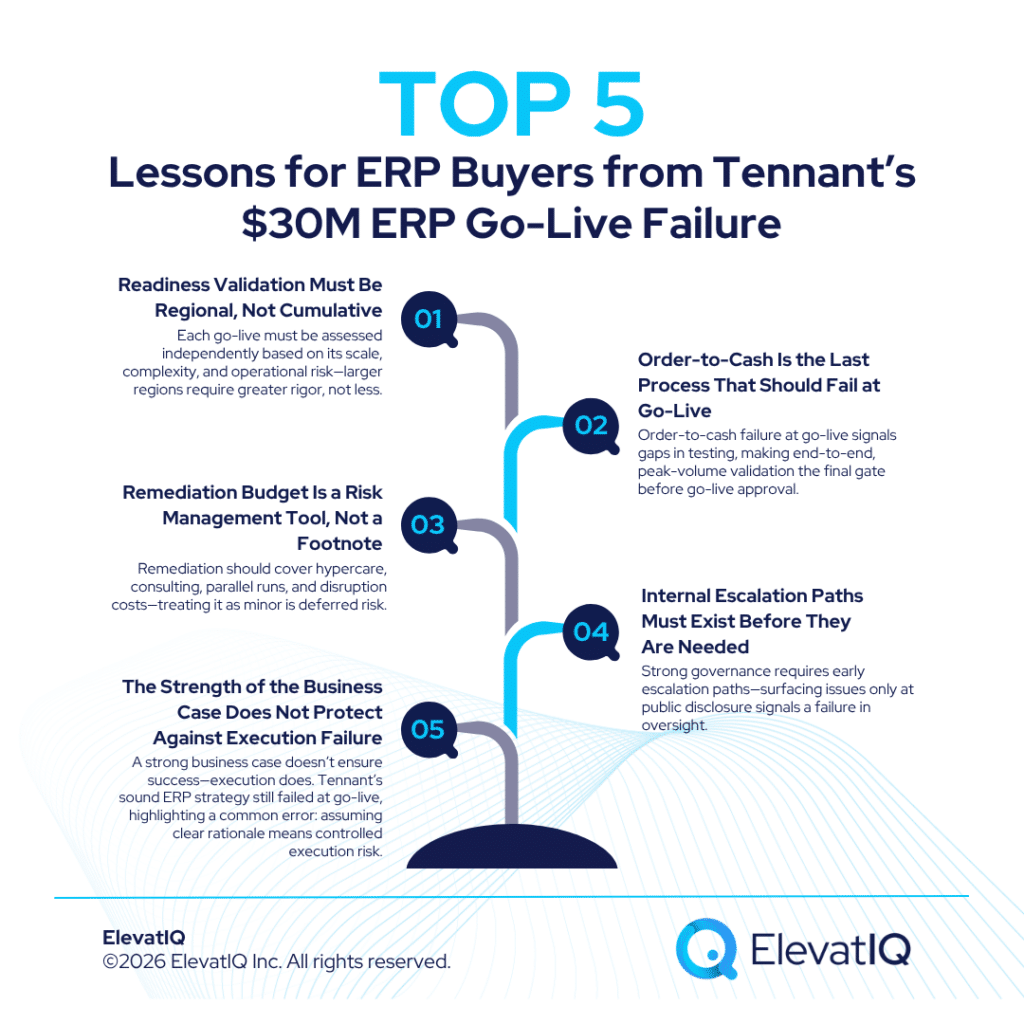

1. Readiness Validation Must Be Regional, Not Cumulative

The North American go-live was preceded by extensive preparation, per the CEO’s own account. The Asia-Pacific success was cited as evidence that the program was proceeding well. Neither was sufficient.

Go-live ERP readiness assessments must be conducted fresh against the specific conditions of each deployment. Its transaction volumes, integration dependencies, cutover complexity, and operational criticality, not inherited from prior phases. The fact that APAC completed without an ERP go-live failure does not reduce the rigor required for North America. In many cases, it should increase it, precisely because North America carries materially higher operational stakes.

2. Order-to-Cash Is the Last Process That Should Fail at Go-Live

The inability to enter orders, ship products, and service customers is a failure in the revenue-generating core of the business. ERP go-live failure in these processes converts immediately and visibly into lost sales, customer relationship damage, and market reaction.

Any ERP program that allows order-to-cash to fail at go-live may indicate gaps in integration testing or cutover validation and an ERP go-live failure in order fulfillment is among the most damaging outcomes possible for a manufacturer. Testing the order-to-cash workflow, including every system that touches a customer order from entry through shipment confirmation under realistic peak-volume conditions should be the final gate before any go-live authorization is granted.

3. Remediation Budget Is a Risk Management Tool, Not a Footnote

Tennant’s remediation costs for 2026 exceeded $20 million against a planned $5 million. A 4x overrun on the remediation line alone, on top of a total program that had already grown from an estimated $75 million to approximately $98 million. This reflects a pattern often observed in failed ERP programs: remediation is budgeted as a small post-go-live support line rather than as a genuine contingency against stabilization failure.

A realistic ERP remediation budget accounts for extended hypercare, emergency consulting, parallel running costs, potential module re-implementation, and the customer-facing costs of fulfillment disruption. Treating remediation as a minor budget item is not conservatism, it is deferred risk.

4. Internal Escalation Paths Must Exist Before They Are Needed

The Tennant CEO’s statement that North America was extensively prepared before go-live, combined with the severity of the failure, raises a question that is relevant to every complex ERP program: at what point was the executive leadership team receiving signals that the North American go-live carried elevated risk, and what were the escalation and decision-making structures that processed those signals?

Clear internal escalation paths and transparent external communication plans should be in place well before go-live. A program governance structure that surfaces problems only at the point of public disclosure has failed its primary purpose.

5. The Strength of the Business Case Does Not Protect Against Execution Failure

Tennant’s consolidation rationale, eliminating eight fragmented ERP instances, building unified digital infrastructure, enabling growth, was sound and publicly stated. The investment was authorized and progressed over multiple years with board involvement. None of that protects the organization from the consequences of an ERP go-live failure in the most operationally critical region.

The business case justifies the investment decision. Execution discipline determines the outcome. They are separate matters, and conflating the two, using the clarity of the rationale as evidence that the execution risk is under control, is one of the most common governance errors in large technology programs.

What This Means for Organizations Currently Mid-Program

For enterprise buyers already in an ERP program, approaching a regional go-live or preparing a North American or full-scale deployment after earlier phases – the Tennant case raises questions that deserve honest answers before the go-live window closes:

- Has a fresh, independent readiness assessment been completed specifically for this deployment, not carried over from the prior phase?

- Has the order-to-cash workflow been stress-tested under peak-volume conditions with all integration dependencies active?

- Does the remediation budget reflect a realistic worst-case stabilization scenario, not just planned hypercare?

- Are internal program health reports providing honest risk visibility to executive leadership, or are they filtered through project team optimism?

- Is the board or audit committee receiving implementation risk updates on a cadence appropriate to the business materiality of the go-live?

None of these questions require an ERP go-live failure to answer. They are commonly considered elements of rigorous program governance, the kind that separates ERP implementations that stabilize quickly from those that generate $52 million in combined revenue and EBITDA impact in a single quarter.

Conclusion

Tennant Company’s ERP go-live failure is a costly, current, and exceptionally well-documented case study in what happens when the largest and most operationally complex deployment in a phased ERP program is not validated to a standard commensurate with its complexity and business criticality. The $30 million in lost sales, the 23.4% single-day stock drop, the paused EMEA rollout, the ongoing securities investigations, and the multi-year distraction from strategic priorities are the measurable cost of that gap.

The company had a sound rationale. It followed a phased approach. It acknowledged the risk publicly. The available evidence suggests the issue was less about strategy and more about execution validation at the point where failure could no longer be contained. For enterprise buyers at any stage of their own ERP journey, this case reinforces what independent ERP advisors emphasize consistently: the business case for transformation is rarely the problem. The problem is almost always in the governance, testing discipline, and escalation structures that determine whether the go-live delivers on that case or undermines it.

ElevatIQ’s enterprise technology selection and implementation advisory services are specifically designed to provide the independent oversight that internal teams – under deadline pressure and organizational momentum, can find difficult to sustain. As independent ERP advisors, ElevatIQ works with organizations to ensure that go-live readiness is assessed against the actual conditions of each deployment, not against the success of the phase that came before it.

ERP Selection: The Ultimate Guide

This is an in-depth guide with over 80 pages and covers every topic as it pertains to ERP selection in sufficient detail to help you make an informed decision.

FAQs

Related Posts: