There is a pattern that surfaces repeatedly in ERP advisory conversations. It rarely comes from organizations that are just starting their evaluation. It comes from organizations that went live twelve to eighteen months ago. Now they are looking at their renewal invoice or a new statement of work, and are trying to understand why the numbers look so different from what was budgeted.

The answer, more often than not, is not fraud or bad faith. It is something more structural. The way modern ERP contracts are designed means that Year 1 is often the most favorable year financially. The costs that matter most, the ones that compound, escalate, and expand. They tend to concentrate in Year 2 and beyond. Hence, understanding ERP contract costs year 2 is something most organizations do too late.

ERP contract costs year 2 surprises are now one of the most consistent themes in post-go-live advisory conversations. Yet almost no organization budgets for them at contract signing, because the Year 1 numbers look manageable. The vendor relationship feels strong after a successful go-live, and the categories driving the escalation often do not appear prominently in the original pricing proposal.

This blog breaks down the three primary drivers of post-go-live ERP cost escalation. Why do they tend to crystallize in Year 2 specifically? And also, what organizations can do to anticipate them before the invoice arrives.

Why Year 1 Feels Affordable

Year 1 of an ERP contract is structured, in most cases, to minimize sticker shock. Initial license or subscription pricing is heavily negotiated, implementation costs are scoped tightly to secure the deal, and consumption charges are low because the system is not yet running at full operational volume. Discounts secured during procurement such as end-of-quarter concessions, bundled module pricing, waived onboarding fees usually apply in Year 1 and rarely carry forward at the same level.

By the time Year 2 begins, the system is live, the organizational dependency on it is real, and the negotiating leverage that existed before contract signing has largely disappeared. That is the environment in which ERP contract costs year 2 take effect.

The Three Drivers of ERP Contract Costs Year 2

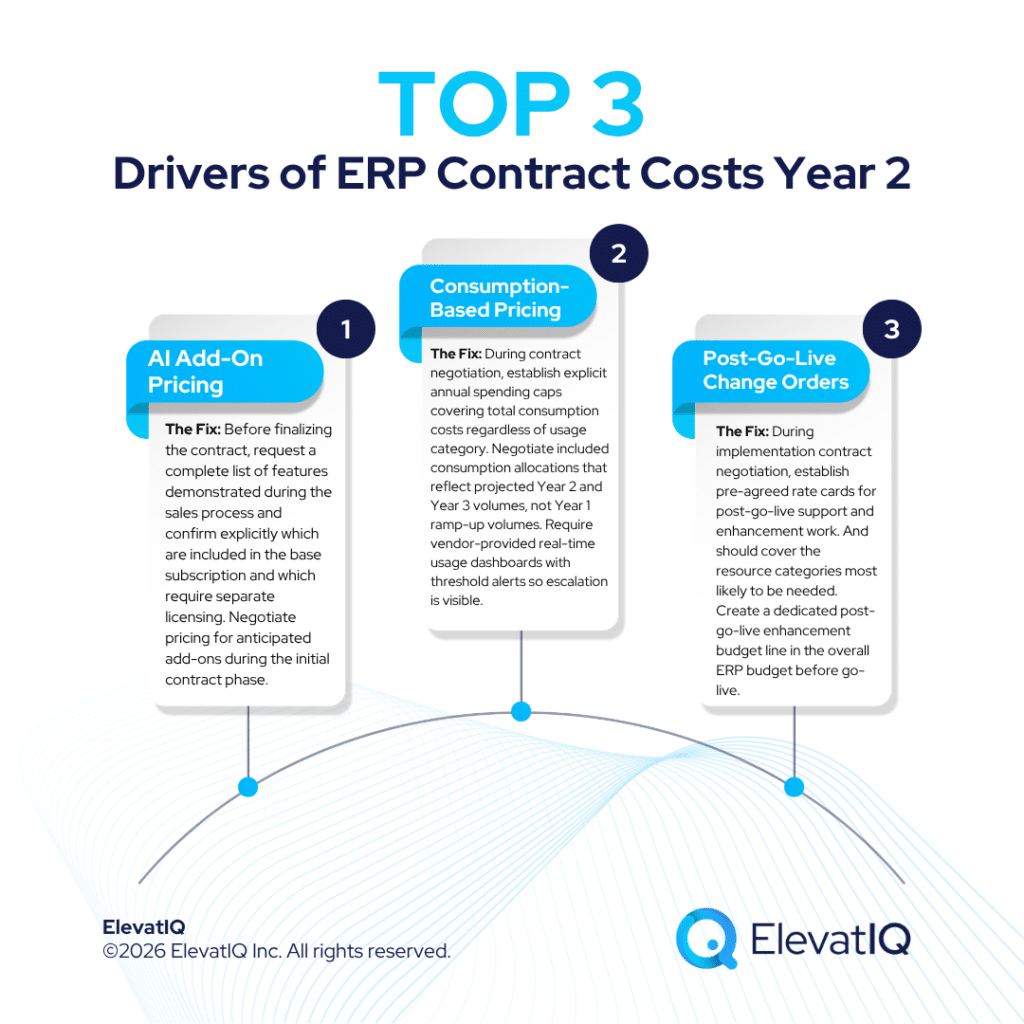

AI Add-On Pricing: The Module That Wasn’t in the Original Scope

Most major ERP vendors have embedded AI-powered features such as intelligent automation, predictive analytics, anomaly detection, natural language interfaces, and generative document creation. Many are positioned as value-adds during the sales process, demonstrated during pre-sale demos as part of the core platform experience. What frequently becomes clear after go-live is that many of these AI capabilities are not included in the base subscription. They are licensed separately, often through an add-on module structure with its own pricing tier.

How this plays out in Year 2:

During ERP implementation, AI features are either turned off or in trial mode, so they do not affect Year 1 costs.

After go-live, end users begin requesting capabilities they saw in the demo which included AI-assisted forecasting, automated three-way match, intelligent expense categorization but only to discover these require additional licensing.

The vendor provides a quote. The quote was not in the original budget. Because the system is live and the business case is now visible, internal pressure to proceed is high but the leverage window closed at original contract signing.

Many vendors have also structured AI capabilities under consumption-based pricing models, meaning costs scale with usage volume rather than a predictable flat rate. This connects directly to the second driver.

The Fix: Before finalizing the original ERP contract, request a complete list of features demonstrated during the sales process and confirm explicitly which are included in the base subscription and which require separate licensing. Negotiate pricing for anticipated add-ons during the initial contract phase. This is the only point at which meaningful price protection is achievable.ve. They will matter far more than the features that work seamlessly.

ERP Selection Requirements Template

This resource provides the template that you need to capture the requirements of different functional areas, processes, and teams.

Consumption-Based Pricing: The Cost That Grows With Your Success

Consumption pricing charges organizations based on actual resource utilization. Like, transaction volumes processed, API calls made, data storage consumed, compute capacity used, and increasingly, AI inference credits generated. In practice, it creates budget unpredictability that almost always manifests most acutely in Year 2.

During ERP implementation and the first months of go-live, transaction volumes are artificially low. Consumption charges in Year 1 reflect this reduced volume and they set a baseline expectation anchored in the budget for Year 2. By Year 2, the system is running at full operational capacity and the consumption charges reflect actual operations, representing a meaningful increase over Year 1 figures.

Common consumption categories that escalate in Year 2:

Consumption Category

Why It Escalates Post-Go-Live

Transaction processing

Full operational volume replaces partial rollout volumes

API call volumes

Integrations run at scale; third-party system connections multiply

Data storage

Transactional history accumulates; archive policies not yet established

AI inference credits

Features enabled post-go-live; usage grows as adoption increases

Report generation

Scheduled reports and ad-hoc queries increase as user confidence grows

By the time charges arrive in Year 2, the conversation about what was or was not contractually protected has already passed its point of influence

The Fix: During ERP contract negotiation, establish explicit annual spending caps covering total consumption costs regardless of usage category. Negotiate included consumption allocations that reflect projected Year 2 and Year 3 volumes, not Year 1 ramp-up volumes. Require vendor-provided real-time usage dashboards with threshold alerts so escalation is visible before the invoice arrives, not after.

ERP System Scorecard Matrix

This resource provides a framework for quantifying the ERP selection process and how to make heterogeneous solutions comparable.

Post-Go-Live Change Orders: The Budget Line Nobody Created

Change orders are perhaps the most predictable source of Year 2 ERP cost escalation. Yet they remain, consistently, the budget line that organizations fail to create. A separate and significant change order dynamic plays out after go-live that tends to be underestimated because it does not look like implementation scope creep. It looks like business-as-usual enhancement requests.

What post-go-live change orders actually look like in Year 2:

A report flagged as a post-go-live enhancement is now actively needed by the finance team for a regulatory requirement.

An integration requires rework because a third-party system was updated and the connection broke.

A new business unit requires configuration and data migration not included in the original scope.

Each generates a change order priced at whatever rate the implementation partner charges for post-go-live work, which in most cases was never negotiated. Organizations arrive at Year 2 with a queue of enhancement requests and an implementation partner no longer operating under competitive pressure.

The Fix: During ERP implementation contract negotiation, establish pre-agreed rate cards for post-go-live support and enhancement work. These rates should be locked for a defined period (typically 24 to 36 months after go-live). And should cover the resource categories most likely to be needed: functional consultants, developers, project managers, and integration specialists. Create a dedicated post-go-live enhancement budget line in the overall ERP budget before go-live, not in response to the first invoice. more likely to support the implementation that follows.

Why Clients Almost Never Budget for This

In advisory conversations, the pattern is consistent: organizations build detailed implementation budgets that account for software licensing, implementation services, data migration, training, and change management. They do not, in most cases, build a Year 2 budget that accounts for the categories described above.

There are structural reasons for this.

First, the budget cycle for ERP implementations tends to be organized around go-live as the financial finish line. Capital expenditure approvals, funding requests, and cost justifications are built around the implementation project. The ongoing operational cost structure including post-go-live escalation, receives comparatively less planning attention because it sits in a future budget cycle.

Second, vendors do not make Year 2 cost visibility easy. AI add-on pricing is often not surfaced clearly in initial proposals. Consumption pricing is quoted at ramp-up volumes that understate Year 2 actuals. Post-go-live support rates are not always included in implementation proposals because implementation partners prefer to quote those separately, closer to when the work begins and leverage has shifted.

Third, there is a natural optimism bias around go-live that compresses concern about future costs. After a successful implementation, the instinct is to celebrate the achievement rather than immediately analyze the forward cost trajectory.

The result is that ERP contract costs year 2 arrive as a surprise not because they were hidden, but because nobody created the model to anticipate them.

Conclusion

Year 1 of an ERP contract is designed to look affordable. Year 2 is where the commercial structure of modern ERP agreements begins to reflect the full ERP contract costs year 2 reality of running a live system at operational scale.

The three drivers: AI add-on pricing, consumption escalation, and post-go-live change orders are not surprises if they are anticipated. They become surprises because most organizations do not have a process for modeling ERP contract costs year 2 before the contract is signed, and because the categories involved are structured in ways that are easy to underestimate during procurement.

The best time to address all three is during the original contract phase. That is when competitive pressure gives buyers leverage over add-on pricing, when consumption cap language can be negotiated into the agreement, and when post-go-live rate cards can be locked. Once the system is live, that leverage is largely gone.

If your organization is currently in ERP contract negotiations or approaching renewal, ElevatIQ’s independent ERP advisory practice works with teams to model total cost of ownership across the full contract lifecycle, including the Year 2 cost structure that most procurement processes leave unmodeled. The advisory engagement is structured with no vendor affiliations and no implementation revenue, so the analysis reflects your commercial interests, not a vendor’s renewal incentives. Post-go-live is not the finish line. For ERP contract costs, it is often the starting line.

ERP Selection: The Ultimate Guide

This is an in-depth guide with over 80 pages and covers every topic as it pertains to ERP selection in sufficient detail to help you make an informed decision.

When enterprise organizations evaluate ERP systems, most of the attention lands on functionality, deployment options, and licensing fees. Support models rarely get the same scrutiny, and vendors often structure offerings accordingly. Over the past several years, ERP vendor support models have undergone a quiet but consequential transformation. One that is reshaping what buyers actually receive once the contract is signed and the implementation is complete.

Understanding these shifts is not optional. For organizations committing to multi-year ERP relationships, often in the seven-figure range. The support model embedded in your agreement directly determines what kind of help you get. Also, how fast, and at what additional cost, when things go wrong or when business needs evolve.

How ERP Vendor Support Models Are Shifting Beyond Pricing

The industry-wide migration from perpetual licensing to subscription-based arrangements is well documented. What is less discussed is how this shift has quietly restructured the nature of support itself.

Under the traditional perpetual license model, annual maintenance fees, typically range from 15 to 22 percent of the original license cost. It usually covers a fairly clear set of entitlements. It often includes product updates, bug fixes, access to support portals, and some level of direct vendor assistance. Buyers understood what they were paying for, even if the fees were substantial.

The subscription model collapses these elements into a single recurring fee and presents it as a simplification. In practice, it is often anything but simple.

Bundled Does Not Mean Comprehensive

Cloud-based ERP subscriptions typically include what vendors describe as a “base level” of support. What falls outside that base level is where buyers frequently encounter surprises. Premium support tiers which offer faster response times, dedicated account management, or access to senior engineers, are increasingly sold as separate add-ons, often at meaningful additional annual cost.

A buyer who compares subscription pricing across vendors may not be comparing equivalent support entitlements at all. One vendor’s standard tier may include 24-hour critical incident response, while another’s requires an upgraded ERP contract to access the same.

Consumption-Based Complexity

Several major ERP vendors have also introduced consumption-based licensing layers within their subscription frameworks. Charges tied to document volumes, API call thresholds, data storage consumption, and indirect user access have become standard features of cloud ERP commercial structures. These mechanics can generate cost exposure that was not anticipated at contract signing. Particularly, as transaction volumes grow or as more third-party systems interact with the ERP.

From a support perspective, this matters because consumption overages often create service disruptions or throttling situations. Resolving them may require navigating vendor escalation paths that are only available to customers on higher-tier support arrangements.

ERP Selection Requirements Template

This resource provides the template that you need to capture the requirements of different functional areas, processes, and teams.

SLA Dilution in ERP Vendor Support Models: The Detail Hiding in Plain Sight

Service level agreements are the contractual backbone of vendor support obligations. Yet in modern ERP agreements, SLA language has evolved in ways that may reduce practical accountability in certain scenarios while maintaining the appearance of strong commitments.

Response Time vs. Resolution Time

One of the most important distinctions buyers overlook is the difference between response time and resolution time. Most ERP vendor SLAs guarantee response times which is the interval between logging a ticket and receiving an acknowledgment. Very few offer enforceable resolution time commitments, meaning the vendor is contractually obligated only to acknowledge the problem, not to fix it within any defined period.

For mission-critical ERP environments, this gap is significant. A system availability issue affecting order processing, financial close, or supply chain operations can remain unresolved for extended periods while remaining technically within SLA compliance.

Tiered Priority Definitions

SLA structures in cloud ERP contracts increasingly rely on vendor-defined priority classifications commonly labeled P1 through P4 or equivalent. The challenge is that what qualifies as a critical incident under the vendor’s internal definitions may not align with what the customer experiences as business-critical. Vendors often retain the right to reclassify incident severity. This can, in some cases, affect response commitments without any breach of contract.

Shared Infrastructure Caveats

In multi-tenant cloud environments, SLA uptime guarantees are often measured at the infrastructure level rather than the application level. A vendor may maintain 99.9 percent platform uptime while specific application modules experience availability issues that fall outside the reported metric. Buyers negotiating ERP agreements should ensure that SLA measurements reflect application-level availability relevant to their operational workflows, not just platform-level metrics.nal complexity increase significantly in subsequent deployments.

ERP System Scorecard Matrix

This resource provides a framework for quantifying the ERP selection process and how to make heterogeneous solutions comparable.

The commercial dynamics behind ERP vendor support models are not difficult to understand once they are surfaced. The problem is that procurement teams and IT leaders often engage with support terms late in the evaluation process. Usually, after commercial positions have already been established.

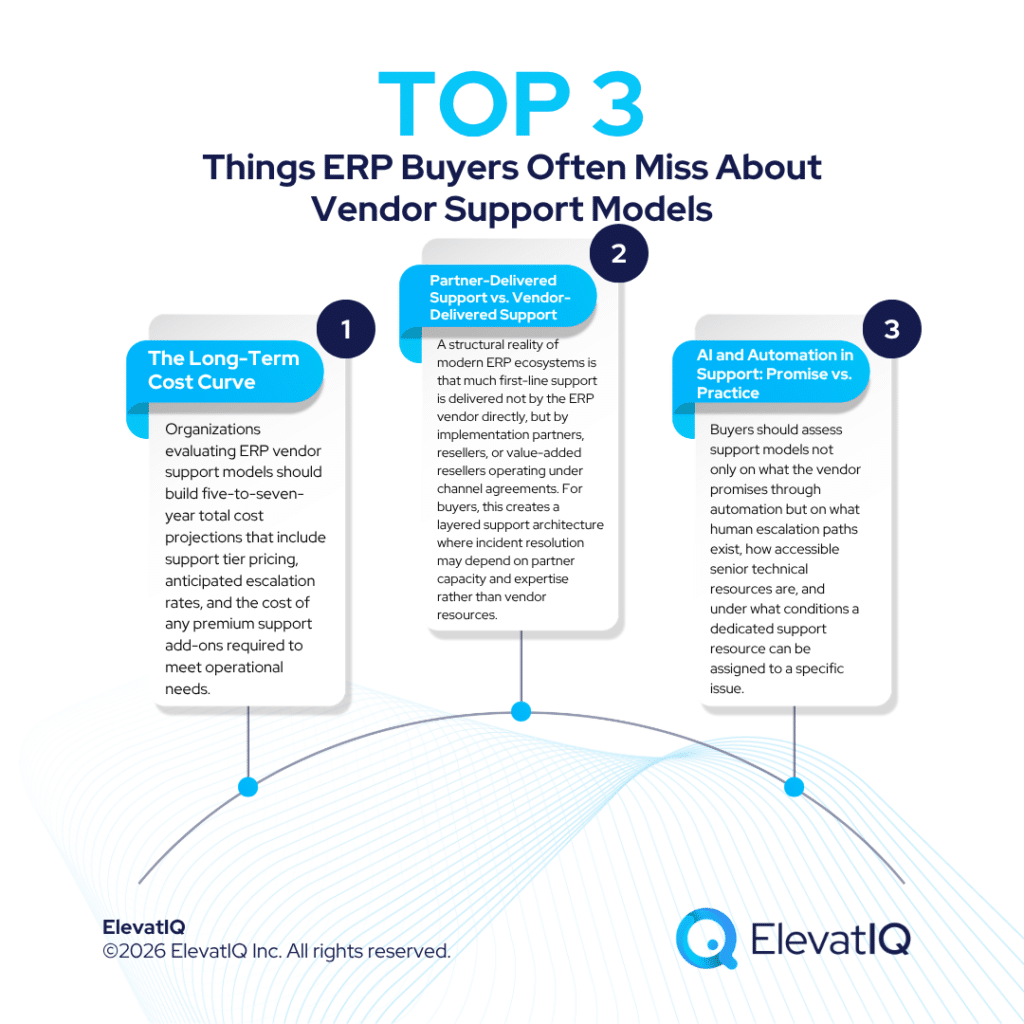

The Long-Term Cost Curve

A frequently cited advantage of subscription models is predictable costs. Over a long horizon, however, subscription costs are not fixed, they are subject to annual escalation clauses, often embedded in ERP contract terms that receive limited attention during negotiation. On-premises annual maintenance fees historically drew scrutiny because they were line items on a perpetual license agreement. Cloud subscription escalations are structurally equivalent but are sometimes framed differently.

Organizations evaluating ERP vendor support models should build five-to-seven-year total cost projections that include support tier pricing, anticipated escalation rates, and the cost of any premium support add-ons required to meet operational needs.

Partner-Delivered Support vs. Vendor-Delivered Support

A structural reality of modern ERP ecosystems is that much first-line support is delivered not by the ERP vendor directly, but by implementation partners, resellers, or value-added resellers operating under channel agreements. For buyers, this creates a layered support architecture where incident resolution may depend on partner capacity and expertise rather than vendor resources.

This arrangement is not inherently problematic, but it requires clarity in the contract about who owns which support obligation, what escalation paths exist to the vendor when the partner cannot resolve an issue, and how response time commitments are measured across the partner-vendor boundary. Evaluating ERP vendor support models means mapping this layered accountability before it becomes an operational problem.

AI and Automation in Support: Promise vs. Practice

ERP vendors are increasingly promoting AI-assisted support capabilities – automated ticket triage, self-service knowledge bases, virtual assistants for common queries. These tools have genuine utility for routine support scenarios. They are less suited to the kind of complex, environment-specific issues that enterprise ERP customers typically face when something goes wrong.

Buyers should assess support models not only on what the vendor promises through automation but on what human escalation paths exist, how accessible senior technical resources are, and under what conditions a dedicated support resource can be assigned to a specific issue.

Key Questions to Ask Before Agreeing to ERP Vendor Support Models

Organizations evaluating ERP vendor support models should bring a specific set of questions into contract negotiations rather than accepting standard terms at face value:

What is explicitly covered under the base support tier, and what requires an upgraded contract?

How does the vendor define incident severity levels, and does the buyer have any input into priority classification?

Are resolution time commitments included anywhere in the SLA, or only response time acknowledgments?

How are SLA metrics measured — at the platform level or at the application and process level?

What escalation path exists if the implementation partner cannot resolve a critical issue?

Are there annual escalation clauses in support pricing, and at what rate?

What data portability and exit support provisions exist if the relationship ends?

These questions do not require adversarial negotiating postures. They represent a reasonable baseline for understanding what an organization is actually purchasing when it commits to an ERP vendor relationship.

Evaluating ERP Vendor Support Models as Part of Vendor Selection

Support model assessment should not occur as a final contract review step. It belongs in the vendor evaluation phase, alongside functional fit and commercial benchmarking.

When comparing ERP vendors, buyers benefit from mapping support tier structures side by side rather than comparing headline subscription prices. The effective cost of a support model that requires a premium add-on to meet operational requirements may be meaningfully higher than a competitor’s all-inclusive arrangement, even if the base subscription appears lower.

Reference checks with existing customers should include specific questions about support experience, not just product satisfaction. Customers who have been through major incidents, upgrade cycles, or environment-specific issues offer the most relevant perspective on what vendor support actually looks like in practice.

The Conclusion

ERP vendor support models are a legitimate and complex area of commercial risk. The shift toward subscription-based delivery has introduced genuine benefits, including reduced infrastructure burden, faster update cycles, and cleaner commercial structures, alongside structural changes in how support obligations are defined and enforced.

Independent ERP advisors can provide meaningful value at this stage of the process, not by negotiating on a buyer’s behalf but by helping organizations understand what standard terms look like across the vendor landscape, where the material risks in specific contract structures are concentrated, and what provisions are genuinely negotiable versus standard boilerplate.

Organizations navigating ERP selection and contract review can benefit from the kind of vendor-neutral perspective that ElevatIQ’s independent advisory practice brings to enterprise technology selection. Understanding what you are actually buying, not just what the sales deck describes, is the foundation of a successful long-term ERP relationship.

ERP Selection: The Ultimate Guide

This is an in-depth guide with over 80 pages and covers every topic as it pertains to ERP selection in sufficient detail to help you make an informed decision.

Are ERP support models negotiable, or are they standardized?

Support tiers and SLA terms vary by vendor and by the size and strategic value of the customer relationship. Larger organizations with significant contract value generally have more leverage to negotiate support terms. That said, standard templates exist for a reason — vendors work from defined commercial structures, and buyers benefit from knowing what is genuinely flexible versus what is policy-level.

What is the difference between a support tier and a maintenance fee?

In on-premises ERP agreements, annual maintenance fees typically cover product updates, bug fixes, and access to support resources. In cloud subscription models, support is often bundled into the subscription but stratified into tiers with different response commitments and resource access levels. The functional distinction matters less than understanding exactly what each structure covers in your specific agreement.

How often do ERP vendors change their support terms?

Vendors reserve the right to update support policies, and cloud-era agreements often include provisions that allow modification of support terms with defined notice periods. Organizations should monitor vendor communications about support policy changes and understand what contractual recourse exists if terms are modified materially.

In the first week of November 2025, Tennant Company (NYSE: TNC) cut over to a new company-wide SAP cloud-based ERP system in North America. It is a Minnesota-based global manufacturer of industrial cleaning equipment, with approximately $1.3 billion in annual revenue. Within days, the business could no longer reliably process or ship customer orders.

The financial damage disclosed on February 24, 2026, was immediate and concrete. They were as follows:

Approximately $30 million in lost net sales in Q4 2025

A $22 million reduction in Q4 adjusted EBITDA

Over $20 million in unplanned remediation costs for 2026, against an original remediation budget of roughly $5 million

Gross profit margin collapsing from 41.3% in Q4 2024 to 34.6% in Q4 2025

Tennant’s stock falling 23.4% in a single trading session, from $82.30 to $63.02. Thus, erasing approximately $343 million in market capitalization

The EMEA go-live, previously scheduled for the following quarter, paused indefinitely

The combined revenue and EBITDA impact in a single quarter was approximately $52 million. The total ERP program investment since 2023 reached approximately $98 million. Multiple securities law firms launched investigations into whether Tennant had accurately represented the project’s progress and risk to investors before the North American disclosure.

An ERP go-live failure of this scale from a company that appeared to follow standard ERP implementation practices, phased its rollout, and acknowledged project risk publicly deserves close examination. Tennant had flagged the project publicly for years. It has acknowledged the risks openly and followed what appeared to be industry best practice in phasing the rollout geographically. The company assessed the Asia-Pacific deployment in September 2025 as successful. Then, it followed with a North American go-live described as extensively prepared. And it still failed.

The Setup: A Legitimate Transformation with a Sound Rationale

Tennant’s ERP consolidation was not an opportunistic initiative. In the Q4 2023 earnings call, CEO Dave Huml articulated the rationale directly. The company was running eight separate ERP systems globally on aging infrastructure. He described that consolidating them onto a single SAP cloud-based platform was essential to the company’s three-year growth strategy. The company estimated the program would cost approximately $75 million in total capital and operating expenditure through 2025, with around $37 million expected in 2024 alone.

The case for consolidation was well-reasoned. Eight fragmented ERP instances make data visibility, operational efficiency, compliance, and cybersecurity governance significantly more difficult to maintain. Bringing the entire enterprise onto a unified platform addresses all of those problems simultaneously.

Throughout 2024 and into 2025, Tennant provided investors with regular progress updates. The company characterized the project as “progressing as we’ve anticipated” and “on time and on budget.” By Q3 2025, it had completed the Asia-Pacific go-live and described it as successful. It had North America underway and scheduled EMEA for the following quarter. Then the Q4 2025 results hit. The ERP go-live failure in North America significantly offset the efficiency gains the consolidation program was designed to deliver over time.

What Actually Went Wrong

In CEO Dave Huml’s own words from the Q4 2025 earnings call:

“Despite a successful go-live in the APAC region in September and extensive preparation in North America, the cut-over of the ERP system in the first week of November introduced severe system functionality issues that limited our ability to enter orders, ship products, and service our customers.”

Three operational functions failed simultaneously at go-live: order entry, product shipment, and customer service. For a manufacturer whose revenue model depends on processing equipment orders and delivering them reliably, this is a failure in the core of the business, not in a peripheral administrative function.

The scale of the disruption indicates this was not a brief cutover hiccup that self-corrected within days. Stabilization challenges extended well beyond the initial go-live window, requiring significant additional investment. The 4x overrun on the original remediation budget is the clearest evidence of that. The company has paused the EMEA deployment indefinitely while North America continues its recovery.

ERP Selection Requirements Template

This resource provides the template that you need to capture the requirements of different functional areas, processes, and teams.

Why the Asia-Pacific Success Did Not Predict the North American Failure

One of the most instructive aspects of the Tennant case is the regional asymmetry. The Asia-Pacific rollout was assessed as successful in September 2025. Eight weeks later, the North American go-live failed.

Organizations commonly observe this pattern in phased ERP programs: earlier phases succeed, while the largest and most complex region experiences ERP go-live failure. Several structural factors explain it:

Transaction volume and complexity. North America is typically the largest revenue region for a global manufacturer. It concentrates the highest order volumes, the densest customer base, and the most complex fulfillment workflows. A system that processes APAC-scale transaction loads without incident may surface entirely different failure modes when exposed to North American peak volumes.

Integration depth. The number of systems, processes, and dependencies connected to the ERP grows with operational scale. North American operations typically carry more integration complexity, more third-party logistics connections, more distributor relationships, more legacy system touchpoints, than earlier-phase deployments.

Process variability. Even within a single ERP program, process configurations differ meaningfully across regions. Workflows validated in APAC may not accurately represent the configuration paths used in North America, meaning that testing results from the earlier go-live carry limited predictive value for the later one.

Cutover execution at scale. The mechanics of cutover including data migration, parallel running, fallback procedures, become materially more complex at North American scale than at APAC scale. Issues that are manageable at a smaller scale can cascade at a larger scale.

As noted in its analysis: phased rollouts do not eliminate risk, they redistribute it. Success in one region does not guarantee stability at scale, particularly when process and geography variability and operational complexity increase significantly in subsequent deployments.

ERP System Scorecard Matrix

This resource provides a framework for quantifying the ERP selection process and how to make heterogeneous solutions comparable.

The Investor Communication Dimension: A New Category of ERP Risk

The Tennant case introduces a risk dimension that most ERP implementation guides do not address: investor communication liability.

Following the February 24 disclosure, securities law firms including Bleichmar Fonti & Auld LLP and Hagens Berman launched investigations into whether Tennant’s prior statements about the ERP rollout accurately represented the project’s progress and risk. The central allegation is that the company characterized the project as on track and the Asia-Pacific go-live as successful in its investor communications, while North America was experiencing or heading toward problems that those communications did not reflect.

These are investigations, not proven findings. They do not establish wrongdoing. But their existence and the speed with which they were launched highlight an important structural point: publicly listed organizations now recognize ERP implementations as material business events subject to the same disclosure expectations as financial restatements and operational incidents.

The gap between internal awareness of ERP go-live failure risk and external communication of that risk is no longer purely a reputational concern. It has become a legal one. For enterprise leaders, including those at privately held companies, where the audience is lenders, private equity sponsors, or boards rather than public investors, the broader principle applies: governance structures must ensure that decision-makers receive timely, honest program health reporting rather than filtered status updates calibrated to maintain organizational momentum.

Five Lessons Enterprise Buyers Must Apply

The Tennant ERP go-live failure is not an isolated anomaly. It reflects failure patterns that appear consistently in large-scale ERP programs. Each of the following lessons is directly traceable to what the Tennant case reveals.

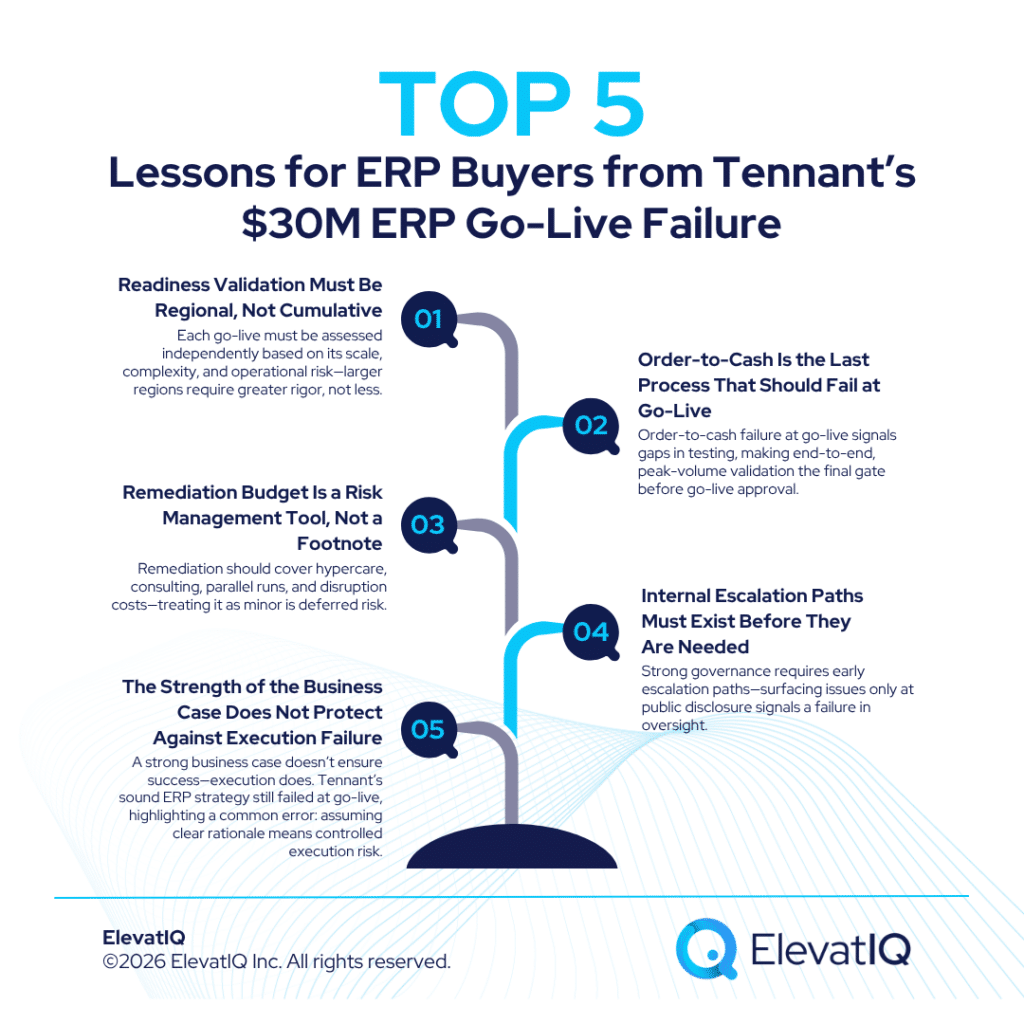

1. Readiness Validation Must Be Regional, Not Cumulative

The North American go-live was preceded by extensive preparation, per the CEO’s own account. The Asia-Pacific success was cited as evidence that the program was proceeding well. Neither was sufficient.

Go-live ERP readiness assessments must be conducted fresh against the specific conditions of each deployment. Its transaction volumes, integration dependencies, cutover complexity, and operational criticality, not inherited from prior phases. The fact that APAC completed without an ERP go-live failure does not reduce the rigor required for North America. In many cases, it should increase it, precisely because North America carries materially higher operational stakes.

2. Order-to-Cash Is the Last Process That Should Fail at Go-Live

The inability to enter orders, ship products, and service customers is a failure in the revenue-generating core of the business. ERP go-live failure in these processes converts immediately and visibly into lost sales, customer relationship damage, and market reaction.

Any ERP program that allows order-to-cash to fail at go-live may indicate gaps in integration testing or cutover validation and an ERP go-live failure in order fulfillment is among the most damaging outcomes possible for a manufacturer. Testing the order-to-cash workflow, including every system that touches a customer order from entry through shipment confirmation under realistic peak-volume conditions should be the final gate before any go-live authorization is granted.

3. Remediation Budget Is a Risk Management Tool, Not a Footnote

Tennant’s remediation costs for 2026 exceeded $20 million against a planned $5 million. A 4x overrun on the remediation line alone, on top of a total program that had already grown from an estimated $75 million to approximately $98 million. This reflects a pattern often observed in failed ERP programs: remediation is budgeted as a small post-go-live support line rather than as a genuine contingency against stabilization failure.

A realistic ERP remediation budget accounts for extended hypercare, emergency consulting, parallel running costs, potential module re-implementation, and the customer-facing costs of fulfillment disruption. Treating remediation as a minor budget item is not conservatism, it is deferred risk.

4. Internal Escalation Paths Must Exist Before They Are Needed

The Tennant CEO’s statement that North America was extensively prepared before go-live, combined with the severity of the failure, raises a question that is relevant to every complex ERP program: at what point was the executive leadership team receiving signals that the North American go-live carried elevated risk, and what were the escalation and decision-making structures that processed those signals?

Clear internal escalation paths and transparent external communication plans should be in place well before go-live. A program governance structure that surfaces problems only at the point of public disclosure has failed its primary purpose.

5. The Strength of the Business Case Does Not Protect Against Execution Failure

Tennant’s consolidation rationale, eliminating eight fragmented ERP instances, building unified digital infrastructure, enabling growth, was sound and publicly stated. The investment was authorized and progressed over multiple years with board involvement. None of that protects the organization from the consequences of an ERP go-live failure in the most operationally critical region.

The business case justifies the investment decision. Execution discipline determines the outcome. They are separate matters, and conflating the two, using the clarity of the rationale as evidence that the execution risk is under control, is one of the most common governance errors in large technology programs.

What This Means for Organizations Currently Mid-Program

For enterprise buyers already in an ERP program, approaching a regional go-live or preparing a North American or full-scale deployment after earlier phases – the Tennant case raises questions that deserve honest answers before the go-live window closes:

Has a fresh, independent readiness assessment been completed specifically for this deployment, not carried over from the prior phase?

Has the order-to-cash workflow been stress-tested under peak-volume conditions with all integration dependencies active?

Does the remediation budget reflect a realistic worst-case stabilization scenario, not just planned hypercare?

Are internal program health reports providing honest risk visibility to executive leadership, or are they filtered through project team optimism?

Is the board or audit committee receiving implementation risk updates on a cadence appropriate to the business materiality of the go-live?

None of these questions require an ERP go-live failure to answer. They are commonly considered elements of rigorous program governance, the kind that separates ERP implementations that stabilize quickly from those that generate $52 million in combined revenue and EBITDA impact in a single quarter.

Conclusion

Tennant Company’s ERP go-live failure is a costly, current, and exceptionally well-documented case study in what happens when the largest and most operationally complex deployment in a phased ERP program is not validated to a standard commensurate with its complexity and business criticality. The $30 million in lost sales, the 23.4% single-day stock drop, the paused EMEA rollout, the ongoing securities investigations, and the multi-year distraction from strategic priorities are the measurable cost of that gap.

The company had a sound rationale. It followed a phased approach. It acknowledged the risk publicly. The available evidence suggests the issue was less about strategy and more about execution validation at the point where failure could no longer be contained. For enterprise buyers at any stage of their own ERP journey, this case reinforces what independent ERP advisors emphasize consistently: the business case for transformation is rarely the problem. The problem is almost always in the governance, testing discipline, and escalation structures that determine whether the go-live delivers on that case or undermines it.

ElevatIQ’s enterprise technology selection and implementation advisory services are specifically designed to provide the independent oversight that internal teams – under deadline pressure and organizational momentum, can find difficult to sustain. As independent ERP advisors, ElevatIQ works with organizations to ensure that go-live readiness is assessed against the actual conditions of each deployment, not against the success of the phase that came before it.

ERP Selection: The Ultimate Guide

This is an in-depth guide with over 80 pages and covers every topic as it pertains to ERP selection in sufficient detail to help you make an informed decision.

Tennant’s Q4 2023 earnings call confirmed the company was consolidating its eight existing ERP systems onto a SAP cloud-based solution as part of a program originally estimated at approximately $75 million through 2025.

What exactly failed during Tennant’s North American go-live?

Per CEO Dave Huml’s statement in the Q4 2025 earnings call, the cutover in the first week of November 2025 introduced severe system functionality issues that limited Tennant’s ability to enter orders, ship products, and service customers. All three represent core revenue-generating operational functions.

How much has the Tennant ERP program cost in total?

The program was originally estimated at approximately $75 million in total capital and operating expenditure. By 2026, total investment since 2023 had reached approximately $98 million, with 2026 remediation costs expected to exceed $20 million against an original plan of roughly $5 million.

When ERP systems go down, the financial consequences accumulate fast. Order processing halts. Financial close cycles stall. Production schedules break. Customer commitments are missed. For organizations running mission-critical operations on a single ERP platform, unplanned downtime is not an inconvenience. It is a direct operational and financial crisis.

Yet when most buyers negotiate ERP contracts, disaster recovery provisions receive far less scrutiny than pricing, licensing terms, or implementation scope. The result is that disaster recovery in ERP contracts is silent or vague. Especially, on exactly the commitments that matter most when something goes wrong.

Disaster recovery in ERP contracts deserves dedicated negotiation effort. This blog covers what buyers need to address – RTO and RPO commitments, backup requirements, cloud provider responsibilities, and the testing rights that determine whether any of it actually works in practice.

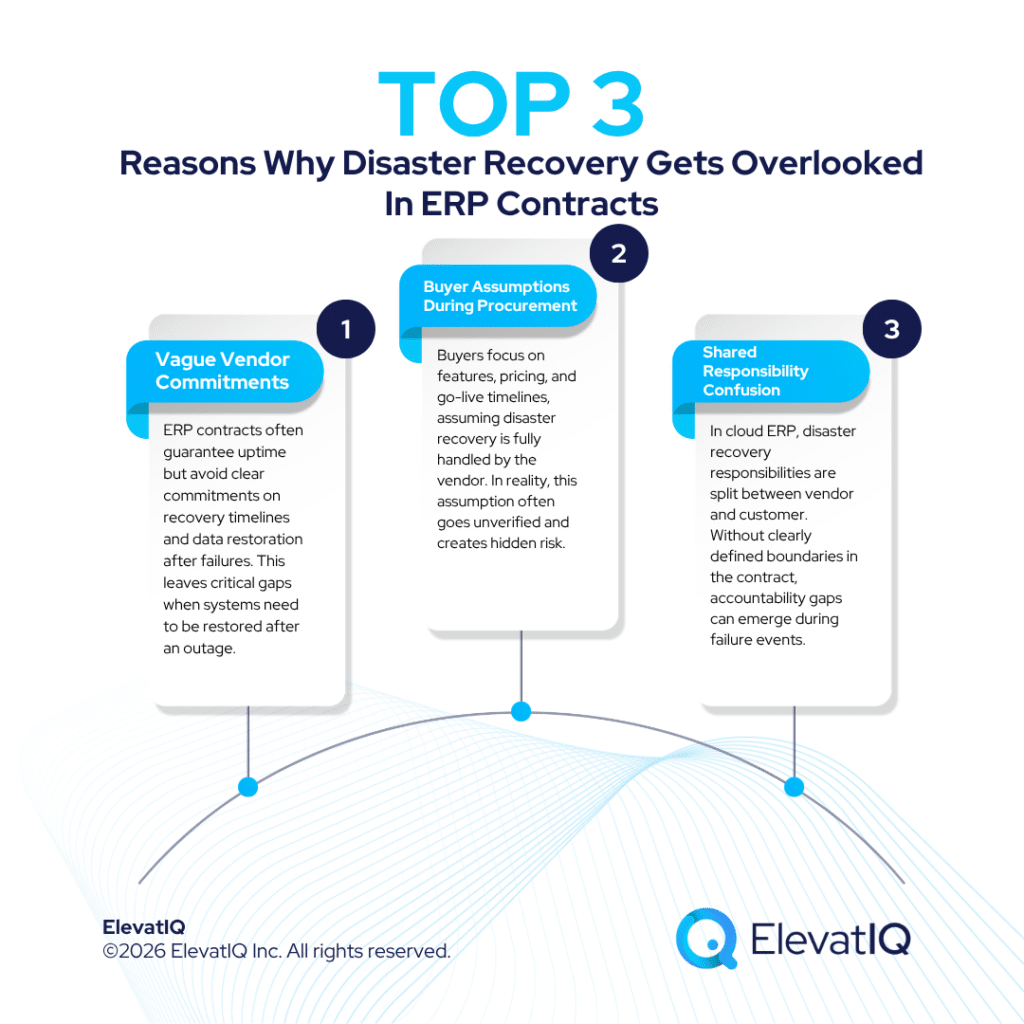

Why Disaster Recovery in ERP Contracts Gets Overlooked

The gap in many ERP contracts is not always accidental. Vendors may benefit from vague language. Standard SaaS agreements typically guarantee infrastructure uptime, the availability of the platform but stop well short of committing to specific data recovery timelines or functional restoration standards after a failure event.

Buyers, focused on features, price, and go-live timelines during contract negotiations, often accept this framing. The assumption, especially for cloud ERP deployments, is that the vendor is handling disaster recovery as part of the service. That assumption is often incorrect, and addressing disaster recovery in ERP contracts before signing is far less costly than discovering the gap after an outage.

The distinction matters most in the cloud context, where the shared responsibility model explicitly divides accountability between vendor and customer. Understanding exactly where that line falls and negotiating contract language that locks it down is a foundational step in any ERP procurement.

RTO and RPO: The Two Numbers That Define Your Risk Exposure

Recovery Time Objective (RTO) and Recovery Point Objective (RPO) are the two core metrics that any discussion of disaster recovery in ERP contracts must address. They are not technical details for the IT team to handle separately, they are business risk decisions that belong in the contract itself.

Recovery Time Objective (RTO) defines the maximum amount of time the ERP system can be offline before the outage becomes operationally unacceptable. It answers the question: how quickly must the system be restored? An RTO of four hours means the vendor is committing to have the system operational within four hours of a declared disaster event.

Recovery Point Objective (RPO) defines the maximum amount of data loss, measured in time, that the organization can tolerate. It answers the question: how current must the data be when we recover? An RPO of one hour means the system will be restored with no more than one hour of transactional data lost.

Both metrics look in different directions from the point of failure. RPO looks backward – how recent was the last recoverable backup? RTO looks forward – how long until systems are back online?

Setting Appropriate Targets for Mission-Critical ERP

Not all ERP modules carry the same criticality, and RTO/RPO targets should reflect that. A financial close system processing period-end entries carries different risk than a secondary reporting module. Buyers should conduct a Business Impact Analysis (BIA) before contract negotiations to understand the operational and financial cost of downtime per hour across core ERP functions. This analysis anchors RTO/RPO discussions in business reality rather than arbitrary benchmarks.

As a general orientation, enterprise-class ERP providers running managed hosting environments may support RPO targets as tight as 30 minutes and RTO windows in the two- to four-hour range for high-priority workloads. However, achieving tighter targets requires both the right infrastructure architecture and explicit contractual commitments, not assumptions. Buyers should press vendors on what specific RTO and RPO figures they can commit to contractually, not just what they claim is technically possible.

What Contract Language Should Capture

Vague language like “best efforts to restore within a reasonable timeframe” is not enforceable and provides no recourse. Disaster recovery in ERP contracts must specify:

Named RTO and RPO figures, expressed in hours or minutes, not qualitative terms

The definition of a “disaster event” that triggers these commitments including whether ransomware, accidental deletion, and partial system failures are covered alongside infrastructure outages

Whether the committed RTO and RPO apply to the full ERP system or only to specific components

Financial remedies – service credits or penalties, that apply if the vendor misses committed recovery targets

Escalation procedures and communication timelines during a declared disaster event

ERP Selection Requirements Template

This resource provides the template that you need to capture the requirements of different functional areas, processes, and teams.

Understanding Cloud Provider Responsibilities: The Shared Responsibility Gap

One of the most consequential misunderstandings in disaster recovery in ERP contracts is the assumption that moving to cloud ERP transfers disaster recovery responsibility to the vendor. It does not, at least not entirely.

Every major cloud provider including those underpinning ERP platforms like SAP S/4HANA Cloud, Oracle Fusion ERP, and Microsoft Dynamics 365 operates under a shared responsibility model. The specifics vary by deployment type, but the general principle is consistent:

The cloud provider is responsible for the availability and resilience of the infrastructure – the physical data centers, the network, the compute and storage layers, and the platform uptime.

The customer retains responsibility for how data is configured, replicated, governed, and recovered at the application and data level.

Oracle has stated this plainly in its cloud documentation: while OCI is responsible for resilience of the cloud, the customer is responsible for resilience in the cloud. Microsoft’s Azure shared responsibility documentation makes the same distinction. Customers who design and implement DR strategies including cross-region replication, failover configurations, and recovery runbooks – are better protected than those who rely on platform-level availability SLAs alone.

For buyers, this means disaster recovery in ERP contracts must address two distinct layers:

Data center redundancy and geographic failover capability

Platform uptime SLA (typically 99.9% or higher, but note this governs availability, not recovery from failure)

Incident notification timelines and communication protocols during outages

Application and data-level commitments (negotiated boundary)

Backup frequency and retention period for the customer’s ERP data

Geographic location of backup copies (same-region vs. geo-redundant)

Who is responsible for executing recovery steps – the vendor’s managed services team, or the customer’s IT organization

Whether the vendor provides a managed DR service as part of the standard subscription or as a separately priced add-on

Many SaaS ERP contracts may not explicitly address the second set of items, leaving buyers to assume coverage they do not have. Explicit contract language assigning responsibility for each layer is essential.

Backup Requirements: Frequency, Retention, and Access

Backup provisions are the operational foundation of any DR commitment. Disaster recovery in ERP contracts should define:

Backup frequency: How often is a full backup of the ERP environment taken? For most enterprise ERP deployments, daily full backups with continuous log archiving between snapshots is commonly considered a baseline approach. Buyers with tighter RPO requirements should ask whether intraday or near-continuous replication is available and contractually committed.

Retention period: How long are backup copies retained? Standard commercial terms often default to 30 days. Organizations with compliance, audit, or regulatory obligations – financial services, healthcare, government contractors, frequently need longer retention periods, sometimes 90 days or more. This needs to be in the contract, not handled as a configuration default that can change.

Geographic redundancy: Are backup copies stored in a separate geographic region from the primary system? Single-region backups are vulnerable to the same regional event that caused the primary outage. Geo-redundant storage ensures that a natural disaster, data center failure, or regional infrastructure incident does not take out both the primary system and its backups simultaneously.

Buyer access to backups: Can the buyer independently access backup data, or must all recovery operations go through the vendor? This matters both for operational control and for scenarios where the vendor relationship has terminated or the vendor has gone out of business. Contracts should guarantee buyer access to backup data regardless of contract status.

ERP System Scorecard Matrix

This resource provides a framework for quantifying the ERP selection process and how to make heterogeneous solutions comparable.

DR Testing Rights: The Provision Most Contracts Omit

Of all the elements of disaster recovery in ERP contracts, DR testing rights are the most commonly absent and their absence can turn a written commitment into an unverified assumption.

A vendor can document robust RTO and RPO targets in a contract. Without regular, verified testing, neither the buyer nor the vendor actually knows whether those targets are achievable. Hardware configurations change. Data volumes grow. Integration dependencies evolve. A DR plan that worked eighteen months ago may not perform the same way today.

DR testing rights that buyers should negotiate into any ERP contract

Annual failover testing: The right to require the vendor to execute a full DR failover test at least once per year, demonstrating that systems can be restored to the contracted RTO and RPO targets under realistic conditions.

Tabletop exercise participation: The right to participate in or independently conduct tabletop exercises that walk through disaster scenarios, validate escalation procedures, and confirm that both vendor and customer teams understand their respective roles.

Access to test results: The right to receive written documentation of DR test outcomes, including whether RTO and RPO targets were met, what issues were identified, and what remediation steps were taken.

Unannounced testing rights: For the most risk-sensitive organizations, the right to request a DR test on reasonable notice – say, 30 days, without having to wait for an annually scheduled exercise.

Remediation obligations: If a DR test reveals that the vendor cannot meet committed RTO or RPO targets, the contract should specify a remediation timeline and an escalation path if issues are not resolved.

The absence of testing rights means the buyer has a paper commitment that has never been verified. For mission-critical ERP systems where downtime costs thousands of dollars per hour, that may not be an acceptable position for many organizations.

On-Premises vs. Cloud ERP: How DR Responsibilities Differ

Disaster recovery in ERP contracts looks different depending on the deployment model, and buyers should approach negotiation accordingly.

Cloud SaaS ERP: The vendor manages infrastructure, platform, and often application-layer backups as part of the service. The risk for buyers is assuming that this coverage is complete without verifying what is and is not included. The shared responsibility gap described above is most pronounced here. Key negotiation focus: defining the exact scope of vendor-managed DR, locked-down RTO/RPO commitments, and testing rights.

Cloud IaaS/PaaS (customer-managed ERP on cloud infrastructure): The buyer is responsible for a broader range of DR decisions such as replication configuration, failover architecture, and recovery runbook design, while the cloud provider manages the underlying infrastructure. Key negotiation focus: infrastructure availability SLAs, support for DR architecture implementation, and contractual clarity on where provider responsibility ends.

On-premises ERP: The buyer owns the full DR stack, but the ERP vendor’s contract still plays a role, specifically around support during recovery events, access to disaster recovery licenses for standby systems, and the vendor’s own obligations if software bugs contributed to a data loss event. Key negotiation focus: DR-specific license terms, support response commitments during outages, and vendor liability for data loss attributable to defective software.

Connecting DR Commitments to Broader Business Continuity Planning

Disaster recovery in ERP contracts does not exist in isolation. ERP is typically one of several interconnected systems such as EDI integrations, financial reporting tools, third-party logistics platforms, CRM, that together enable business operations. A contractual DR commitment that covers the ERP platform but not its integration dependencies leaves the organization partially protected at best.

Buyers should ensure that DR contract provisions account for:

Integration recovery sequencing: In what order must interconnected systems be restored for the ERP to function usefully after a failover?

Dependency mapping: Which third-party systems or APIs does the ERP rely on, and what are those providers’ DR commitments?

Data reconciliation procedures: After recovery, how are data discrepancies between the ERP and connected systems identified and resolved?

These cross-system considerations are frequently outside the scope of standard vendor contract templates, which is exactly why they need to be raised explicitly during negotiation.

Conclusion

Disaster recovery in ERP contracts is not a technical afterthought – it is a direct expression of how much operational risk an organization is willing to accept without contractual protection. ERP systems are among the most mission-critical platforms in any enterprise. The cost of unplanned downtime measured in lost transactions, missed reporting deadlines, and broken customer commitments, is too high to leave DR provisions to standard vendor language.

Buyers who invest the effort to negotiate specific RTO and RPO targets, clear backup requirements, defined cloud provider responsibilities, and enforceable testing rights are far better positioned than those who accept default contract terms and discover the gaps only when something goes wrong. Getting disaster recovery in ERP contracts right is not inherently complex but it does require knowing what to ask for.

Working with independent ERP advisors who have evaluated DR provisions across dozens of vendor agreements gives organizations the benchmarking intelligence to know what is achievable, what is negotiable, and what red flags to watch for in standard vendor templates. ElevatIQ’s enterprise technology selection and IT procurement advisory services include contract review support specifically designed to surface gaps in disaster recovery, SLA, and business continuity provisions helping organizations secure the protections they need from independent ERP advisors who negotiate vendor agreements every day.

ERP Selection: The Ultimate Guide

This is an in-depth guide with over 80 pages and covers every topic as it pertains to ERP selection in sufficient detail to help you make an informed decision.

What are RTO and RPO, and why are they critical in ERP contracts?

RTO (Recovery Time Objective) defines how quickly the ERP system must be restored after a disruption, while RPO (Recovery Point Objective) defines how much data loss is acceptable. These are not just technical metrics—they directly determine business risk. Without clearly defined and contractually committed RTO and RPO targets, organizations have no guarantee on recovery timelines or data integrity after an outage.

Does moving to cloud ERP mean the vendor fully handles disaster recovery?

No. Cloud ERP operates under a shared responsibility model. While vendors manage infrastructure availability, customers are often still responsible for aspects like data configuration, replication, and recovery processes. Many contracts do not clearly define these boundaries, which can leave critical gaps unless explicitly addressed during negotiation.

Why are disaster recovery testing rights important in ERP contracts?

Testing rights ensure that disaster recovery plans actually work in practice, not just on paper. Without regular failover testing, tabletop exercises, and access to test results, there is no way to verify whether the vendor can meet committed RTO and RPO targets. For mission-critical ERP systems, untested recovery plans can create significant operational and financial risk during real outages.

Signing an ERP implementation contract is one of the highest-stakes procurement decisions an organization will make. Yet many buyers focus almost entirely on software licensing costs and give far less scrutiny to the one document that determines who absorbs the financial pain when things go wrong: the implementation services agreement itself.

The choice between a fixed price and a time and materials (T&M) ERP implementation contract is rarely about which model is inherently superior. It is about which one is appropriate for your specific project conditions and whether you have negotiated enough protections within that model to keep risk where it belongs.

This blog examines both ERP implementation contract models in depth, covering how each allocates risk, what change order provisions should look like, and what buyers should demand regardless of which model they choose.

What the Two Contract Models Actually Mean

Before evaluating risk, it helps to be precise about what each model commits both parties to.

Fixed Price Contracts

Under a fixed price model, the vendor agrees to deliver a defined scope of work for a predetermined total fee. Payments are typically structured around project milestones, for example, a portion at kickoff, another at user acceptance testing, and the final amount at go-live.

Key characteristics:

Scope, deliverables, and timeline are defined and locked before work begins

The vendor absorbs the financial risk if their estimates are wrong or work takes longer than planned

Any requirement not explicitly covered in the contract scope is subject to a formal change order and additional fees

Vendors typically build a risk contingency buffer into their pricing to protect against uncertainty

The last point matters more than most buyers realize. Because vendors are accepting delivery risk, they price that risk into the contract. Fixed price contracts tend to include contingency buffers for unknowns, which can inflate the project cost by 15% to 30% or more, and the client pays this premium regardless of whether the risks ever materialize.

Time and Materials Contracts

Under a T&M model, the buyer pays for actual hours worked at pre-agreed rates, plus any direct project expenses. There is no guaranteed final price; the total depends entirely on how long the work takes.

Key characteristics:

The scope can evolve throughout the project without formal ERP renegotiation

The buyer absorbs the financial risk if implementation takes longer than expected

Vendor invoices are based on actual time spent, requiring the buyer to monitor hours closely

There may be limited direct incentive for vendors to optimize efficiency, since they are paid for the time and materials utilized, without the same direct time-based incentive to complete the project quickly.

The flexibility of T&M suits projects where requirements are not fully defined or where significant customization is anticipated. However, without spending controls built into the contract, T&M can expose buyers to runaway costs when scope expands or technical complexity proves greater than expected.

The vendor carries execution risk – if they underestimate effort, they absorb the cost overrun. This sounds like a buyer-friendly arrangement, and in theory it is. In practice, vendors manage this risk through two mechanisms that shift it back to buyers:

Scope inflation at the change order stage. Because any work not explicitly described in the contract can be classified as out-of-scope, vendors may have an incentive to define scope narrowly and then bill for changes. Vague or incomplete ERP requirements documentation creates fertile ground for change order disputes.

Risk premium pricing. Vendors build uncertainty buffers into fixed price bids. If the project runs smoothly, the buyer may have paid more than the actual delivery cost. If disputes arise over scope, the buyer may face both the premium already paid and additional change order fees.

Under a Time and Materials Contract

The buyer carries cost risk, if the project expands or takes longer, their costs rise proportionally. Industry studies suggest that approximately 47% of ERP implementation projects experience cost overruns.Separately, among organizations that did exceed their budgets, nearly 35% said the initial project scope was expanded NetSuite – the exact dynamic that T&M contracts leave financially unprotected by default.

Vendors operating under T&M also face reduced accountability for delivery quality. Since they are compensated regardless of outcomes, contractual performance standards and acceptance criteria become even more important under this model than under fixed price.

ERP System Scorecard Matrix

This resource provides a framework for quantifying the ERP selection process and how to make heterogeneous solutions comparable.

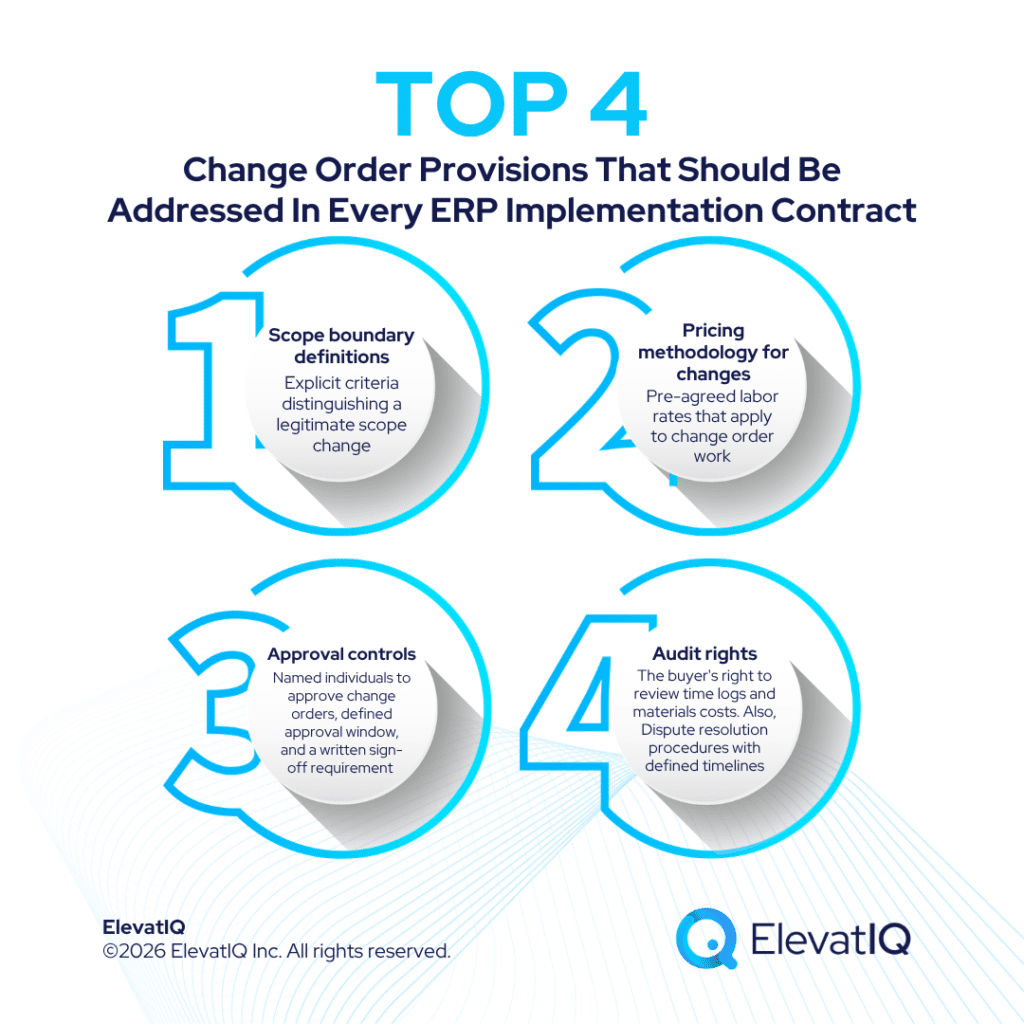

Change Order Procedures: Where Contracts Succeed or Fail

Regardless of which model a buyer selects, change order procedures are where the practical protection lives. Both ERP implementation contract models are vulnerable to disputes when change order language is weak. Under a fixed price contract, every request the vendor classifies as outside the original scope becomes a potential change order. Without clear definitions of what constitutes a legitimate change versus a clarification of vague scope, vendors can impose additional fees on items a reasonable buyer would consider implied by the original requirements.

Under a T&M contract, scope changes have no formal gate – work simply continues. Without a structured change request process, it becomes difficult to track what was originally agreed upon, what was added, and at whose request. Strong change order provisions should address the following regardless of which ERP implementation contract model is in use:

Scope boundary definitions

Explicit criteria distinguishing a legitimate scope change from a clarification or correction of ambiguous vendor documentation

A process for the buyer to dispute vendor claims that work falls outside original scope

Pricing methodology for changes

Pre-agreed labor rates that apply to change order work, preventing vendors from charging premium rates for out-of-scope items

A cap on change order markup or overhead percentages

Written itemized estimates for each change request before work begins

Approval and authorization controls

Named individuals on the buyer side with authority to approve change orders

A defined approval window (e.g., five business days) to prevent delays from authorization bottlenecks

A written sign-off requirement before any out-of-scope work commences

Audit rights

The buyer’s right to review time logs and materials costs supporting any change order invoice

Dispute resolution procedures with defined timelines if a buyer contests a change order

One practical note: change order disputes are commonly cited as a major source of conflict in ERP projects. High-profile cases like the MillerCoors vs. HCL dispute which resulted in a $100 million lawsuit before eventual settlement, were attributed by outside observers to contracts that were loosely defined and left substantial room for disagreement about what each party had committed to deliver.

Cost Controls Buyers Should Negotiate Into Either Model

Beyond change order language, buyers can negotiate additional protections into any ERP implementation contract – fixed price or T&M alike.

For Fixed Price Contracts

Scope completeness warranty: Require the vendor to warrant that their fixed price proposal reflects a complete and accurate assessment of the work required to meet documented requirements. This limits the vendor’s ability to reclassify work as out of scope based on their own estimating errors.

Acceptance criteria with teeth: Define functional acceptance criteria that must be met before milestone payments are released. “Substantially conforms to documentation” is not an acceptable standard. Require documented test cases with pass/fail criteria.

Change order volume caps: Negotiate a threshold beyond which aggregate change order costs trigger a contract renegotiation or an ERP independent assessment. This prevents a nominally fixed price contract from becoming variable in practice through uncontrolled scope additions.

For Time and Materials Contracts

Not-to-Exceed (NTE) clauses: A Not-to-Exceed cap establishes a ceiling on total billable hours or total project cost, beyond which the vendor cannot charge without a formal, buyer-approved change order. This hybrid approach offers the best of both worlds – the project operates on a flexible T&M basis, but is bound by a firm budget ceiling, providing the adaptability of T&M with the budget protection of a fixed price model.

Spending authorization thresholds: Require vendor notification when cumulative costs reach defined percentages of the project budget, for example, at 50%, 75%, and 90% of the NTE cap. This builds early warning into the contract rather than surfacing overruns only at invoice time.

Role-based rate schedules: Pre-agree specific hourly rates for each resource category (project manager, functional consultant, technical consultant, integration specialist). This prevents vendors from staffing projects with senior resources at premium rates for work that does not require that level of seniority.

Time-log transparency: When internal resources run low, organizations frequently use a software vendor’s services team or third-party consultants more than planned, with experienced ERP consultants typically running $150–175 per hour plus travel expenses. NetSuite requires weekly time-log submissions broken down by task, resource, and project phase, which gives buyers the visibility to govern these costs proactively.

Which Model Is Right for Your ERP Project?

There is no universally correct answer. It depends on the state of your requirements and your organization’s capacity to govern the implementation actively.

Fixed price contracts are generally more appropriate when:

Requirements are fully documented, stable, and unlikely to change significantly during implementation

The organization needs budget certainty for internal planning or board-level approvals

The buyer has limited bandwidth to monitor vendor activity on a day-to-day basis

Time and materials contracts are generally more appropriate when:

Requirements are still evolving or involve significant business process redesign

The project involves heavy customization or complex integrations where effort is genuinely hard to estimate upfront

The organization has strong internal project management capability and can monitor vendor hours closely

Speed of iteration is a priority and formal change order cycles would slow progress unacceptably

A hybrid approach – T&M for early discovery and design phases, transitioning to fixed price for defined build phases – is also worth considering for complex ERP implementations. This structure is well-suited to large ERP rollouts: fixed price for well-scoped modules where the vendor has repeatable implementation patterns, and T&M for integration, customization, and cutover support.It allows requirements to stabilize through T&M engagement before locking a price, reducing the vendor’s justification for large contingency buffers.

The Question Buyers Often Miss

Most discussions about ERP implementation contract models focus on which model is less risky. The more useful question is: which model are you actually equipped to manage?

A fixed price contract with weak scope definitions and no change order controls does not protect a buyer. Neither does a T&M contract with no spending caps and no time-log visibility requirements. The contract model is a framework. The protection comes from the specific language within it.

The MillerCoors case underscores a broader lesson: when ERP contracts are poorly defined and loosely based, neither party has a clear definition of success or responsibility – setting the stage for disputes where the cost of legal escalation can quickly eclipse the original project investment.Organizations that lack internal expertise in technology contract negotiation frequently discover this distinction only after costs have escalated.

Conclusion

Both fixed price and T&M ERP implementation contract models offer legitimate paths to a well-governed ERP project – under the right conditions and with the right provisions in place. Fixed price shifts execution risk to the vendor but requires precise scope documentation and disciplined change order controls to prevent that protection from eroding. T&M preserves flexibility but demands NTE caps, rate transparency, and active buyer oversight to remain cost-controlled.

For most mid-market and enterprise buyers, the single most important step is engaging qualified support before the contract is signed, not after disputes arise. Independent ERP advisors – those without financial relationships with the software vendors or system integrators on the other side of the table – are best positioned to evaluate which model fits a specific project and negotiate the provisions that make it enforceable.

ElevatIQ’s enterprise technology selection and IT procurement advisory services support buyers through both the vendor selection process and the contract negotiation stage. Working as independent ERP advisors, the team reviews proposed contract structures, flags risk allocation gaps, and helps organizations secure language that improves vendor accountability regardless of which pricing model is on the table.

ERP Selection: The Ultimate Guide

This is an in-depth guide with over 80 pages and covers every topic as it pertains to ERP selection in sufficient detail to help you make an informed decision.

Which ERP implementation contract model is less risky: fixed price or time and materials?

Neither model is inherently less risky—it depends on the project and how well the contract is structured. Fixed price shifts execution risk to the vendor but can lead to higher upfront costs and change order disputes if scope is unclear. Time and materials offers flexibility but shifts cost risk to the buyer unless controls like not-to-exceed (NTE) caps and spending thresholds are in place.

Why do change orders become a major problem in ERP implementation contracts?

Change orders often become a problem because of unclear scope definitions. In fixed price contracts, vendors may classify additional work as out-of-scope and charge extra. In time and materials contracts, changes can accumulate without clear tracking or approval. Without strong change order procedures—such as defined scope boundaries, pricing rules, and approval controls—costs can escalate quickly and lead to disputes.

What protections should buyers negotiate regardless of the contract model?

Buyers should negotiate protections such as clear acceptance criteria, transparent pricing for changes, audit rights over vendor billing, and defined approval processes for additional work. For fixed price contracts, this includes scope completeness warranties and limits on change order volume. For time and materials, key protections include NTE caps, rate controls, and time-log transparency to prevent cost overruns.

Software license audits are often perceived as extending beyond pure compliance checks. For most large ERP vendors, they can also serve as a revenue-generating mechanism. That is, a structured process for identifying gaps between what customers technically owe under a complex licensing agreement and what they actually paid for. Understanding ERP audit rights before you sign a contract is one of the most financially consequential steps an organization can take. Yet it rarely receives the attention it deserves during procurement.

This blog breaks down how vendor audit clauses work. What makes them dangerous, and what ERP audit rights protections buyers should negotiate. Especially, before they find themselves on the receiving end of a multi-million dollar true-up demand.

Why ERP Vendors Are Auditing More Aggressively Than Ever

Software license audits are not new. But the frequency and financial stakes have shifted considerably in recent years. Industry data published in 2025 indicates that 62% of companies faced software vendor audits in 2024. Thus, up by 40% the previous year. For organizations with more than 5,000 employees, that figure climbed to 66%. The same research found that nearly one in three organizations incurred financial liabilities exceeding one million dollars from audits in 2024. This is more than three times the share from just two years prior.

The drivers behind this surge are not difficult to identify. Enterprise software vendors face consistent pressure to grow revenue year over year. And audits have become a reliable mechanism for achieving that. Especially in mature markets where new customer acquisition has slowed. When a vendor’s quarterly earnings fall short of analyst expectations, audit activity may increase. The relationship is not coincidental.

Oracle, SAP, and VMware (under Broadcom) have consistently ranked among the most active audit initiators in the enterprise software market. Each brings a distinct approach. Oracle has long been known for aggressive enforcement around database and Java licensing. SAP is particularly active around indirect access and integration usage. And, Broadcom’s acquisition of VMware triggered a significant escalation in audit activity alongside sweeping licensing model changes. Vendor audit teams are often embedded within the sales organization and incentivized to convert findings into revenue-generating amendments. A structural fact that should inform how buyers approach every audit interaction.

What ERP Audit Rights Clauses Actually Say

Most enterprise ERP contracts contain an audit rights clause. This grants the vendor the ability to examine a customer’s systems and usage data to verify licensing compliance. These clauses are typically presented as standard, non-negotiable provisions. In practice, many are neither.

Standard audit rights language tends to be broad and buyer-unfavorable. It may grant the vendor the right to conduct audits with little advance notice, at any time, and any frequency. Also, using audit methodologies and tools of the vendor’s own choosing. The clause may also specify that any identified shortfall must be remediated at current list prices rather than the discounted rates the customer originally negotiated.

Providers have inserted audit right language within clients’ contracts, providing legal authority to conduct audits of a client’s environment using both human and technical tools. Also, including scripts that listen to a customer’s environment and generate reports identifying potential non-compliance. This automatically places the client in a defensive position.

There is also a deliberate ambiguity problem. ERP contract language can sometimes be ambiguous regarding permissible use. Customers often find architecture-based compliance the most difficult area to monitor and govern. A common example involves connecting an ERP system to development and test environments, or linking it to a CRM platform via API. Scenarios that many buyers assume are standard practice, but that some vendors can characterize as unlicensed usage.

The Indirect Access Problem

No audit trigger has generated more unexpected costs for ERP customers than indirect access. This refers to any scenario where an external system – a third-party application, a web portal, a robotic process automation tool, or a custom integration- accesses ERP functionality without going through a direct, licensed user login.